EXECUTIVE SUMMARY

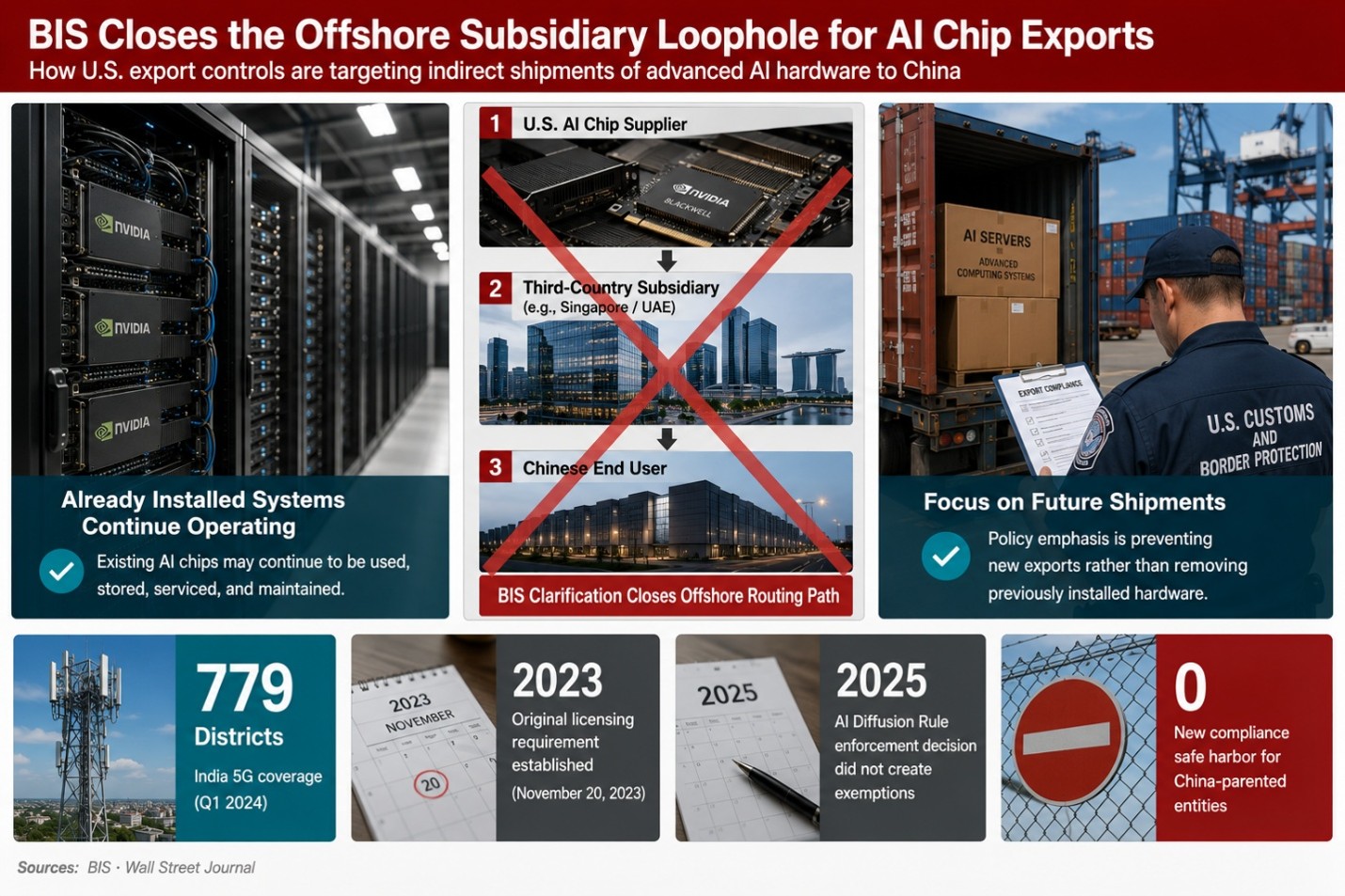

On Sunday, May 31, 2026, the US Bureau of Industry and Security (BIS) issued a guidance that confirmed a simple but powerful idea: the chip export licence rule follows a company’s ultimate parent, not its postal address [BIS]. So now, any firm headquartered in China, or whose ultimate parent sits in China or Macau, needs a licence to receive advanced chips, even if the buying entity is located in Singapore, Malaysia or anywhere else [Holland & Knight]. The real story is not the rule itself. It is what the rule quietly admits, that Blackwell-class chips have already been reaching China through offshore subsidiaries, and that buyers who already have these chips need not stop using them. And here is the contradiction: while one hand of the government is closing this back door, the other hand opened a front door in January by allowing H200 chip sales to China, a move that the Council on Foreign Relations calls “strategically incoherent and unenforceable” [CFR].

STRUCTURED ANALYSIS

Read the guidance for what it admits, not just what it orders

In simple terms, the law part is not new. The licence requirement was first created in November 2023 and only moved around in the rulebook later. The guidance only says clearly that this rule was always there, and that the 2025 decision to not enforce the AI Diffusion Rule never gave any free pass to China-parented companies.

But notice two things hiding inside the guidance. First, BIS would not bother releasing a clarification on a Sunday unless offshore subsidiaries were actually being used as the route. So, this is, in effect, a quiet confession. The Wall Street Journal had already reported that Chinese buyers were getting systems with Nvidia’s Blackwell chips by routing them through third-party entities in nearby countries [WSJ]. The guidance simply shuts that door.

Second, and this is very important for compliance teams, BIS told “bona fide operators of data centers” that they need not “cease the ongoing use, storage, disposal, or servicing” of chips they already have, until further notice [BIS]. Read it plainly. The government is stopping new shipments but allowing the already-installed chips to keep running. In other words, the focus is on stopping the next shipment, not taking back the last one.

The second-order effect: a control regime arguing with itself

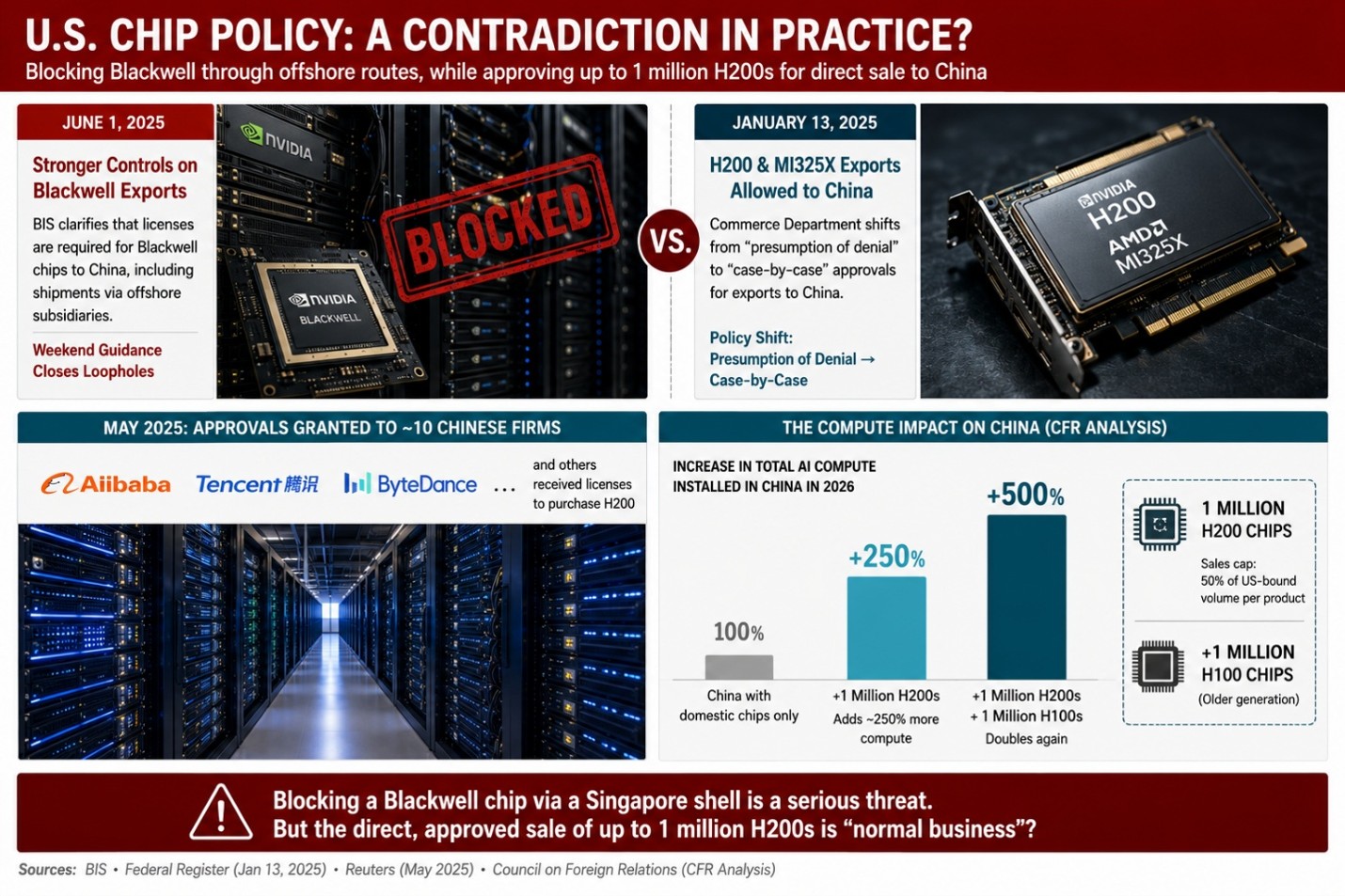

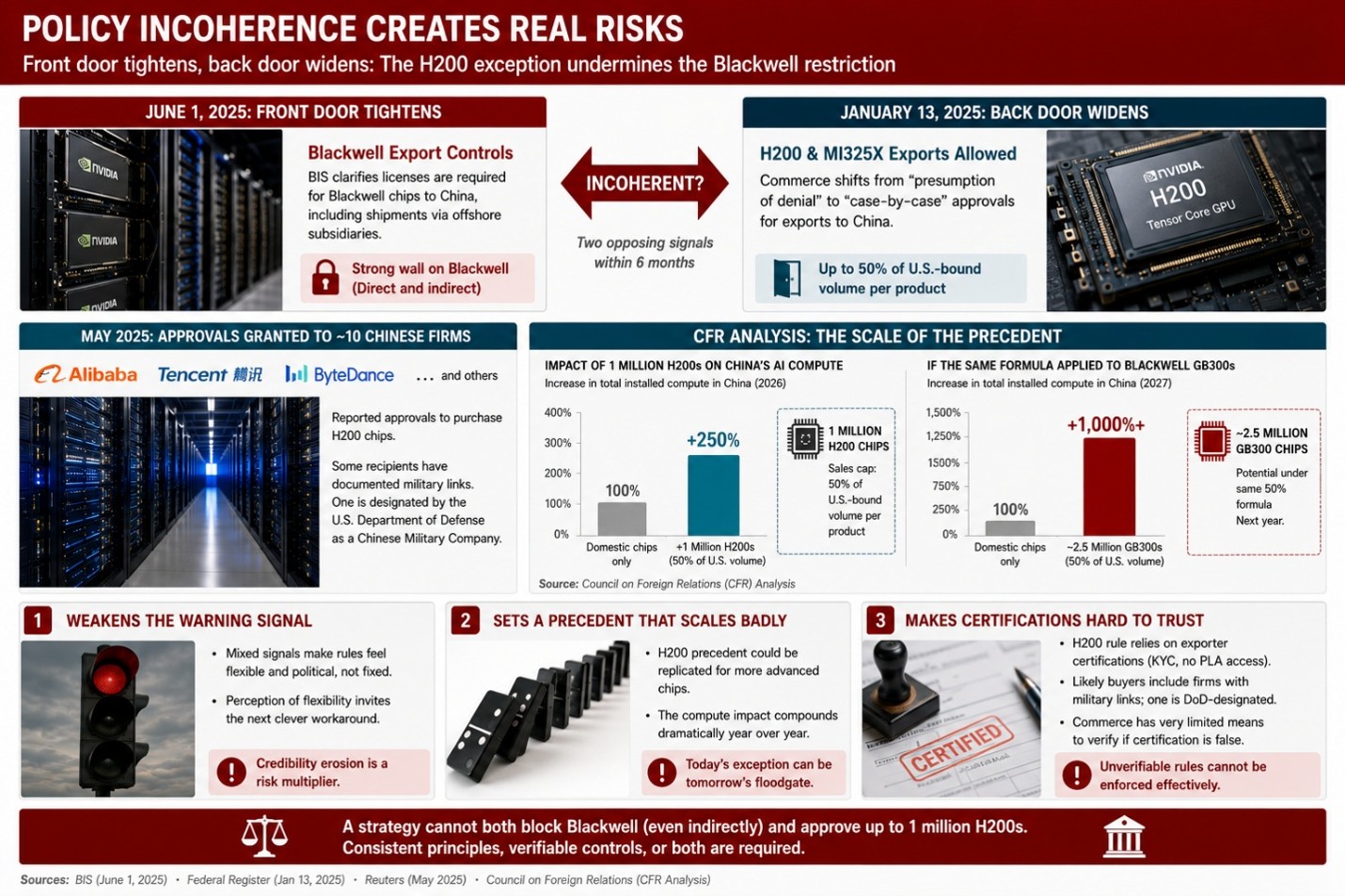

This is where the policy starts to fight with itself. On June 1, BIS is putting up a strong wall to keep Blackwell chips out of Chinese hands, even through offshore companies. But on January 13, the same Commerce Department had published a rule allowing the export of H200 and AMD MI325X-class chips to China, shifting from “presumption of denial” to “case-by-case” approval [Federal Register]. By May, around ten Chinese firms, including Alibaba, Tencent and ByteDance, were cleared to buy the H200 [Reuters].

The CFR analysis gives the number that matters here. The H200 rule caps China sales at 50 percent of US-bound volume per product, which works out to roughly one million H200 chips. CFR’s finding is that one million H200s would increase the total AI compute installed in China in 2026 by about 250 percent, compared to a China depending only on its own domestic chips [CFR]. Add a million older H100 chips on top and that number doubles again.

So, the same government treats a Blackwell chip routed through a Singapore shell as a serious threat worth a weekend bulletin, but treats the direct, approved sale of a million H200s as normal business. Both cannot be the real strategy at the same time.

Why “strategically incoherent” is the correct diagnosis

This incoherence is not just talk. It creates three real problems that policy and strategy teams must plan for.

It weakens the warning signal. When the front door tightens and the back door widens in the same six months, companies start to feel the rules are flexible and political, not fixed. That feeling itself becomes a risk, because it invites the next clever workaround.

It sets a precedent that scales badly. CFR’s sharpest point is this: if the same H200 formula, 50 percent of US volume, were applied to Blackwell GB300 chips next year, it could clear roughly 2.5 million GB300s, raising China’s 2027 installed compute by more than 1,000 percent [CFR]. So the June 1 Blackwell wall is holding a line that the January logic is already pushing against from behind.

It makes the certifications hard to trust. The H200 rule asks exporters to certify strong KYC and no PLA access, even though the likely buyers are cloud firms with documented military links, and one of them is named by the US Department of Defense as a Chinese Military Company [CFR]. And Commerce has very few ways to prove that any such certification is knowingly false. A rule that cannot be checked properly cannot be enforced properly.

Pressure-testing the contrarian case

To be fair to BIS, the two positions can be reconciled on one reading: tier the technology. Allow “legacy” H200-class chips with conditions, but block frontier Blackwell-class chips fully, including via subsidiaries. On paper, this is a sensible design. The problem is that the gap between “legacy” and “frontier” has shrunk so much that even one million units of the allowed tier gives China very large total compute. The tiering idea assumes a big generational moat that sheer volume simply washes away. This is the empirical heart of CFR’s argument, and corporate strategists should test this assumption in their own models rather than accept it blindly.

STRATEGIC RECOMMENDATIONS

- For compliance leaders:Redesign your screening around the ultimate-parent test, not the ship-to address, and do it now. Treat beneficial-ownership tracing through layered offshore structures as a core skill. Separately, if you serve data centres, build a strong “bona fide operator” file now, before BIS defines the term, possibly against you.

- For corporate strategy:Model the split openly. Assume China-facing frontier revenue is structurally limited and politically shaky, while “legacy”-tier revenue is allowed but precedent-setting and reputationally risky. Do not build a revenue plan assuming today’s permissive mood survives the next administration or the next enforcement cycle.

- For policy professionals:Frame the debate honestly. The real question is not “open or closed”. It is whether a tiered system can hold when the permitted tier delivers frontier-level total compute. June 1 and January 13 are the same policy arguing with itself, and fixing it needs one clear objective.

ASSUMPTIONS AND CAVEATS: This reflects the BIS guidance dated May 31, 2026 [BIS] and the January 13, 2026 H200 rule [Federal Register], plus CFR’s published estimates. The 250 percent and 1,000 percent figures rest on stated assumptions about US shipment volumes and a China-domestic-only baseline, so treat them as directional, not exact. The “bona fide operator” exception is undefined, and whether guidance can do the work of formal rulemakingsS is contestable. This is decision-support, not legal advice. Please confirm any transaction decision with qualified export-control counsel.