Exploring the technologies, investment priorities, and infrastructure strategies shaping the next generation of hydropower.

Hydropower is often treated as the old part of the renewable energy mix. That view is becoming outdated. The sector may not be growing as fast as solar or wind, but its role in the power system is becoming more important, not less.

In 2024, hydropower generated around 4,500 TWh of electricity, equal to roughly 14% of global power generation IEA. It remains the world’s largest source of renewable electricity and continues to provide something that solar and wind cannot always offer: controllable, dispatchable power. As grids absorb more variable renewable energy, hydropower is being repositioned as a balancing asset, a storage asset, and a reliability asset.

Hydropower’s Share May Fall, but Its Strategic Value Is Rising

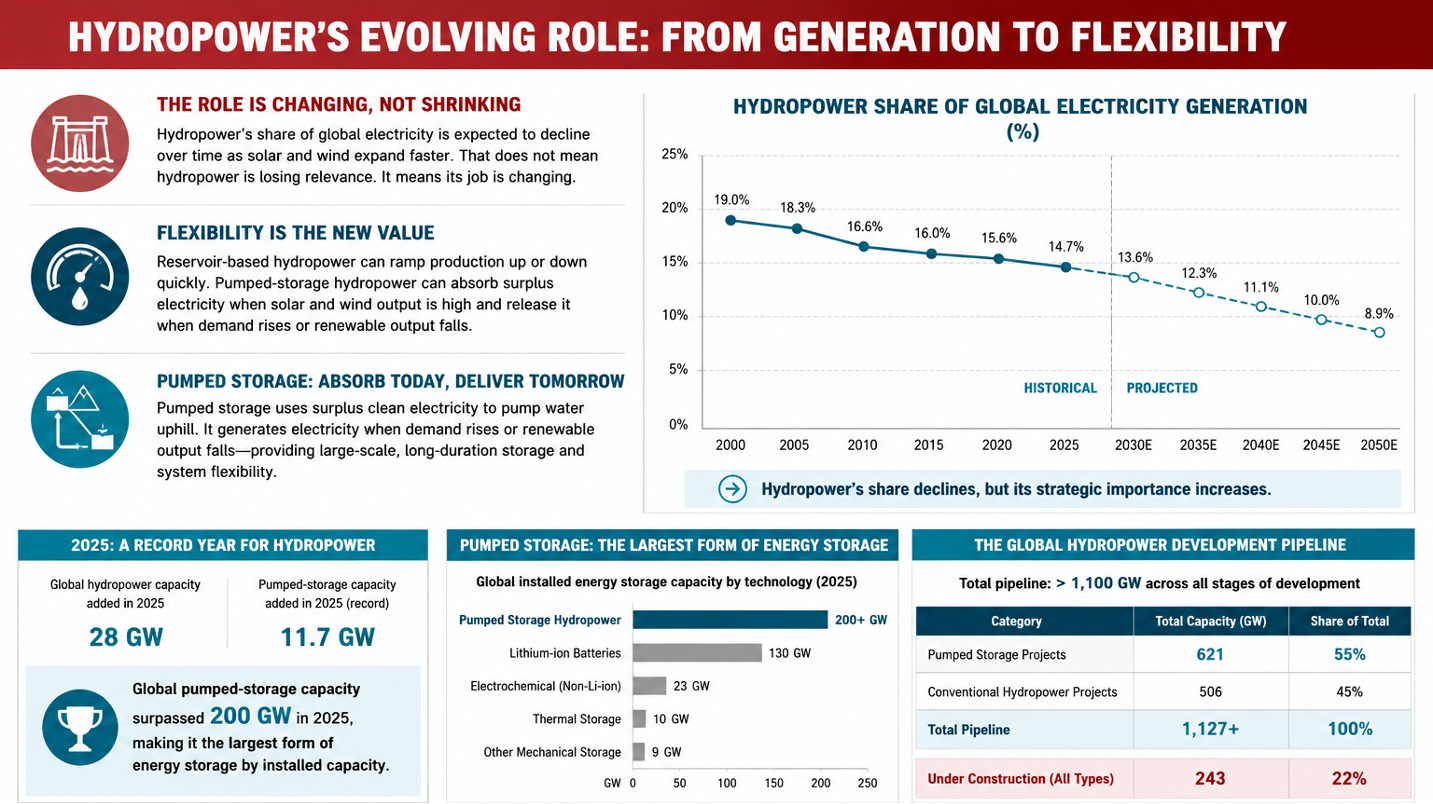

Hydropower’s share of global electricity is expected to decline over time as solar and wind capacity expands faster. That does not mean hydropower is losing relevance. It means its job is changing. For decades, hydropower was valued mainly for bulk electricity generation. Going forward, it will increasingly be valued for flexibility. Reservoir-based hydropower can ramp production up or down quickly. Pumped-storage hydropower can absorb surplus electricity when solar and wind output is high and release it when demand rises or renewable output falls.

This is why pumped storage is becoming central to power system planning. The International Hydropower Association reported that global hydropower capacity grew by 28 GW in 2025, including a record 11.7 GW of pumped storage. Pumped storage capacity also crossed 200 GW worldwide, making it the largest form of energy storage by installed capacity IHA 2026 World Hydropower Outlook.

The global development pipeline now stands at more than 1,100 GW, including 621 GW of pumped-storage projects. That pipeline shows where the market is heading: countries are no longer looking at hydropower only as a renewable generation source. They are looking at it as long-duration storage and strategic grid infrastructure.

Ageing Assets Create a Large Modernization Market

The biggest near-term opportunity may not be new dams. It may be old dams. A large share of global hydropower capacity was built decades ago. Many plants still generate power reliably, but their turbines, generators, control systems, sensors, and grid interfaces were not designed for today’s electricity market. They were built for a slower, more predictable power system. Today’s grid needs fast response, better forecasting, remote operation, and higher availability.

This creates a strong case for modernization. Refurbishing an existing hydropower plant is often faster, less risky, and less controversial than building a new project. It can also improve output without requiring a completely new reservoir or large-scale land acquisition.

The economics are compelling. Upgrading electromechanical equipment can increase output by up to 20%, while larger civil works such as intake improvements, dam heightening, and flow optimization can raise output further. Adding generation to existing dams or upgrading existing hydropower schemes can be far cheaper than building a new storage-equipped project.

This is where suppliers of turbines, control systems, sensors, digital twins, and predictive maintenance platforms will find a large addressable market. Plant owners are not only looking for more megawatts. They are looking for better uptime, lower operating cost, safer operations, and faster grid response.

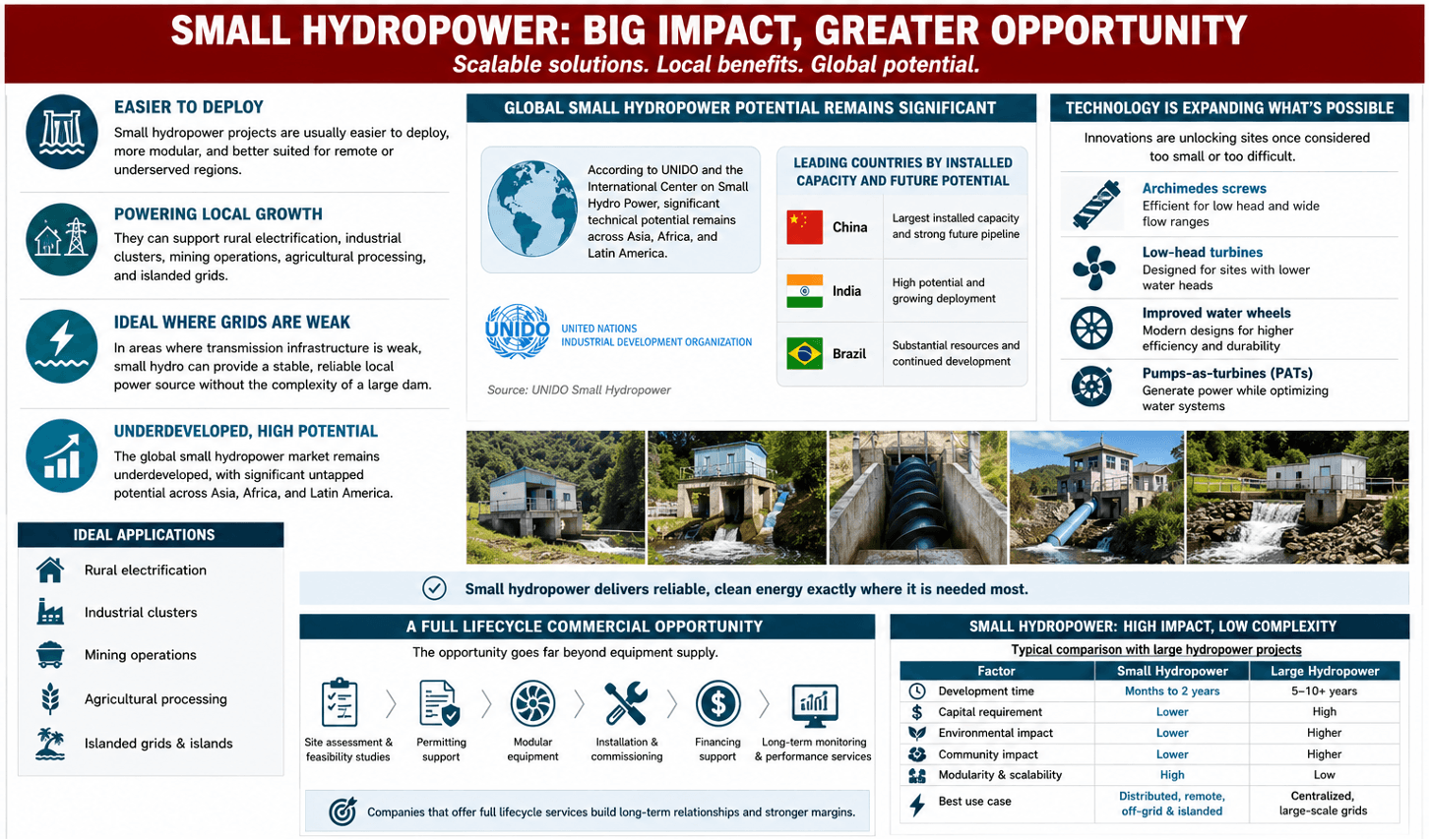

Small Hydropower Remains an Underdeveloped Market

Large dams attract most of the attention, but small hydropower deserves a closer look. Small hydropower projects are usually easier to deploy, more modular, and better suited for remote or underserved regions. They can support rural electrification, industrial clusters, mining operations, agricultural processing, and islanded grids. In areas where transmission infrastructure is weak, small hydro can provide a stable local power source without the complexity of a large dam.

The global small hydropower market remains underdeveloped. The UNIDO and International Center on Small Hydro Power’s global work shows that small hydropower potential remains significant across Asia, Africa, and Latin America UNIDO Small Hydropower. China, India, and Brazil remain among the most important countries for installed small hydropower capacity and future potential.

Technology is also improving the case for smaller systems. Archimedes screws, low-head turbines, improved water wheels, and pumps-as-turbines are helping developers serve sites that were once considered too small or too difficult. For emerging markets, this matters because many viable sites are not large enough to justify a conventional utility-scale hydro project.

The commercial opportunity is not limited to equipment supply. Developers need engineering, site assessment, permitting support, modular equipment, installation, commissioning, financing support, and long-term monitoring. Companies that can offer full lifecycle services will have an advantage over vendors selling only standalone components.

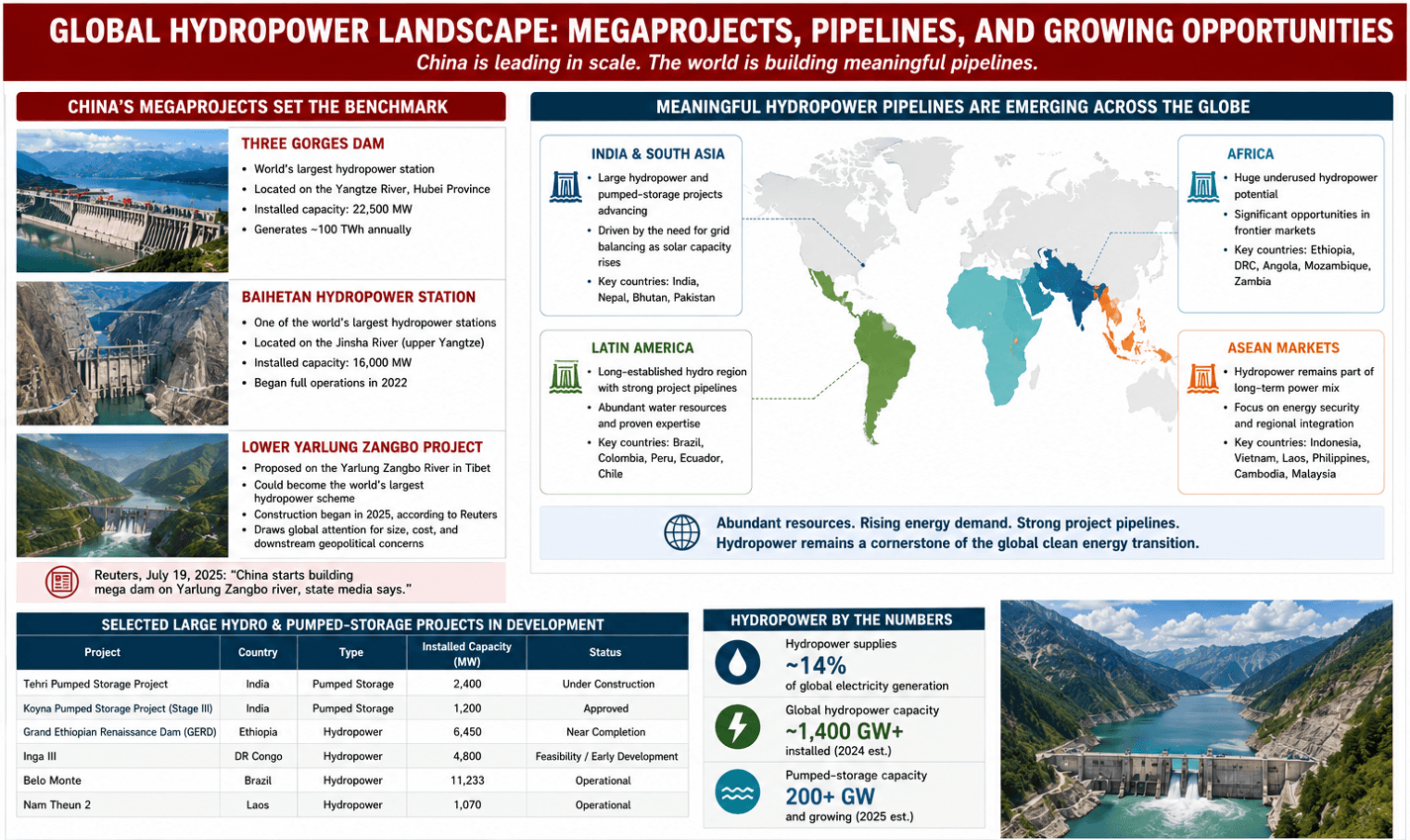

China Will Remain the Largest Market, but the Opportunity Is Broader

China continues to dominate global hydropower development. In 2025, it accounted for more than 40% of global capacity additions and had more than 300 GW of hydropower under construction, including 218 GW of pumped storage IHA 2026 World Hydropower Outlook.

China’s scale is visible in its megaprojects. The Three Gorges Dam remains the world’s best-known hydropower asset, while Baihetan has become one of the world’s largest hydropower stations. The lower Yarlung Zangbo project has also drawn global attention because of its size, cost, and downstream geopolitical concerns. Reuters reported in 2025 that construction had begun on the project, which could become the world’s largest hydropower scheme Reuters.

Outside China, several regions are building meaningful pipelines. India and South Asia are moving forward with large hydropower and pumped-storage projects, supported by the need for grid balancing as solar capacity rises. Africa has huge underused hydropower potential, especially in Ethiopia and the Democratic Republic of Congo. Latin America remains a major hydro region, led by Brazil, Colombia, Peru, and Ecuador. ASEAN markets such as Indonesia, Vietnam, and Laos also continue to evaluate hydropower as part of their long-term power mix.

The opportunity is real, but so are the constraints. Hydropower projects face long permitting timelines, financing challenges, environmental scrutiny, resettlement issues, and climate-related water risks. In many markets, investors will favour projects that use existing dams, smaller footprints, or pumped-storage designs with lower social and ecological disruption.

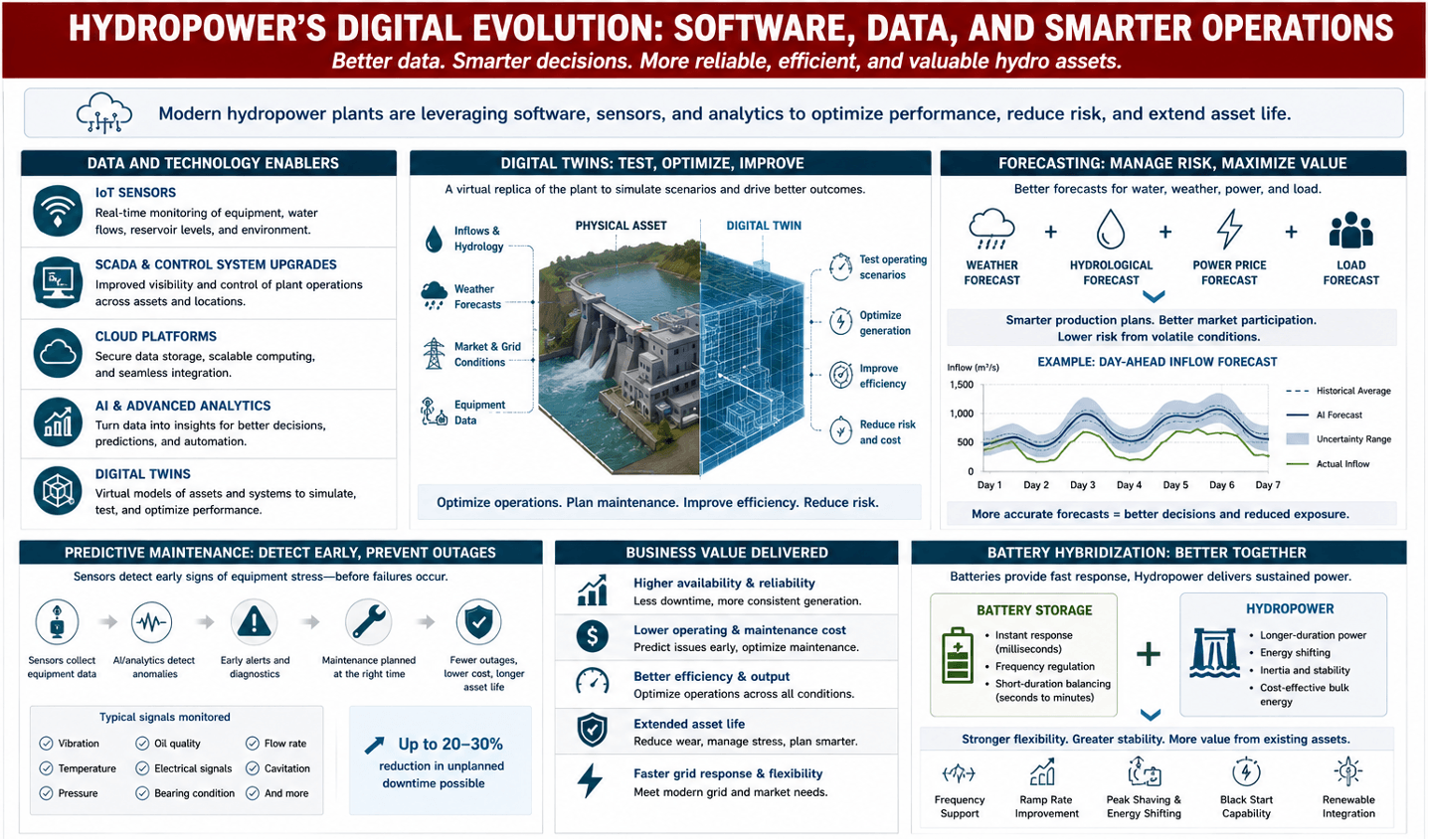

Digital Technology Is Changing How Hydropower Plants Are Run

Hydropower is becoming a software and data story as much as an engineering story. Modern plants need better visibility into water flows, turbine performance, sedimentation, weather risk, reservoir levels, and grid demand. AI-based analytics, IoT sensors, SCADA upgrades, cloud platforms, and digital twins are now being used to improve maintenance planning and operational decision-making.

Predictive maintenance is one of the clearest use cases. Sensors can detect vibration, temperature changes, pressure shifts, and other early signs of equipment stress. This allows operators to address problems before they cause outages. For older plants, these tools can extend asset life and reduce downtime.

Digital twins are also gaining traction. By creating a virtual model of a plant, operators can test different operating scenarios, compare output under different flow conditions, and identify efficiency improvements without disrupting actual operations.

Forecasting is another important area. Weather volatility is now a core business risk for hydro operators. Droughts, sudden floods, and irregular rainfall can directly affect generation, dam safety, and power trading. Companies such as ENFOR offer hydro, weather, power, and load forecasting tools that help operators plan production and manage market exposure.

Battery hybridization is also becoming more relevant. Batteries can respond instantly to short-term frequency changes, while hydropower provides longer-duration backup. In some systems, the combination can improve flexibility and widen the operating range of existing hydro assets.

What This Means for Investors and Industry Players

The investment thesis for hydropower is changing. The strongest opportunities through 2035 are unlikely to be limited to building new large dams. They will sit across modernization, pumped storage, small hydropower, and digital operations.

For equipment manufacturers, the key market will be refurbishment: turbines, generators, control systems, sensors, automation, and grid integration. For software and analytics companies, the opportunity lies in forecasting, digital twins, predictive maintenance, and remote operation. For project developers and financiers, the most attractive projects will be those that balance clean energy value with lower environmental and social risk.

Hydropower is not a fading renewable category. It is becoming a critical support system for renewable-heavy grids. Solar and wind will continue to grow faster, but they need balancing, storage, and reliability. Hydropower can provide all three.

The next decade will reward companies that understand this shift. The market will not be won only by those who build the biggest dams. It will be won by those who modernize existing assets, deploy smaller systems where they make sense, and use data to make hydropower more flexible, reliable, and commercially useful.

Conclusion

Hydropower’s future will not be defined only by how much new capacity the world can build. It will be defined by how intelligently existing and new assets are used in a more renewable-heavy power system.

As solar and wind continue to expand, grids will need dependable sources that can balance supply, store energy, and respond quickly to changing demand. Hydropower is well placed to play that role, especially through pumped storage, plant modernization, small-scale deployment, and digital operating systems.

For emerging markets, the opportunity is particularly important. Many countries still have ageing hydropower fleets, underused small hydro potential, and growing demand for reliable clean power. The winners will be those who move beyond traditional dam development and focus on higher-value opportunities: refurbishing old assets, improving plant flexibility, using data to reduce downtime, and designing projects with lower environmental and social risk.

Hydropower is not a legacy technology losing relevance. It is becoming one of the enabling platforms for the next phase of clean energy growth. The next decade will reward companies, investors, and governments that treat hydropower not just as a renewable power source, but as strategic grid infrastructure.