Introduction

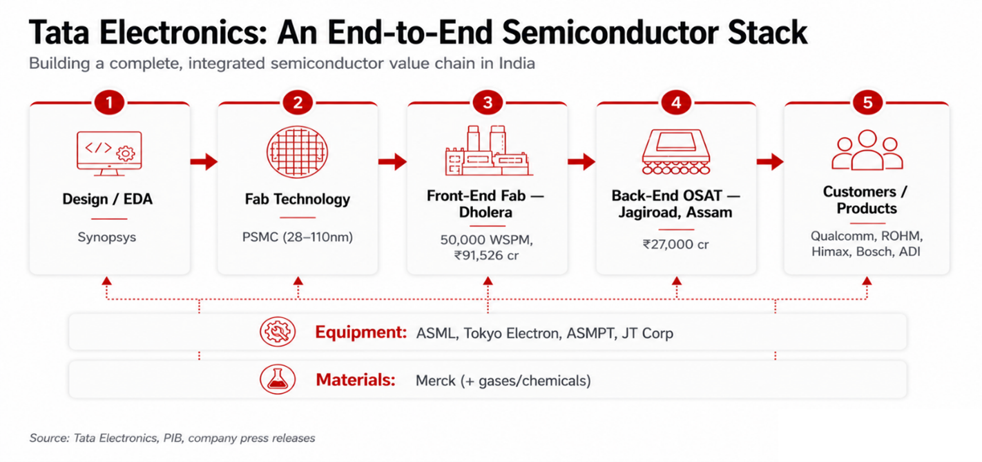

Most first-time entrants into semiconductor manufacturing make one large bet, typically a single fab, and then struggle for years to surround it with the tools, materials, customers, and talent a chip plant actually requires. Tata Electronics Private Limited (TEPL) has taken the opposite approach. It has moved on every layer of the value chain simultaneously: front-end fabrication, back-end packaging, lithography and process tools, ultra-pure materials, electronic design automation, anchor customers, downstream electronics manufacturing through acquisitions, and a workforce pipeline. The result is one of the most densely partnered industrial build-outs in recent Indian history. This article maps that ecosystem in full, partner by partner, and assesses what it adds up to.

The Two Physical Anchors

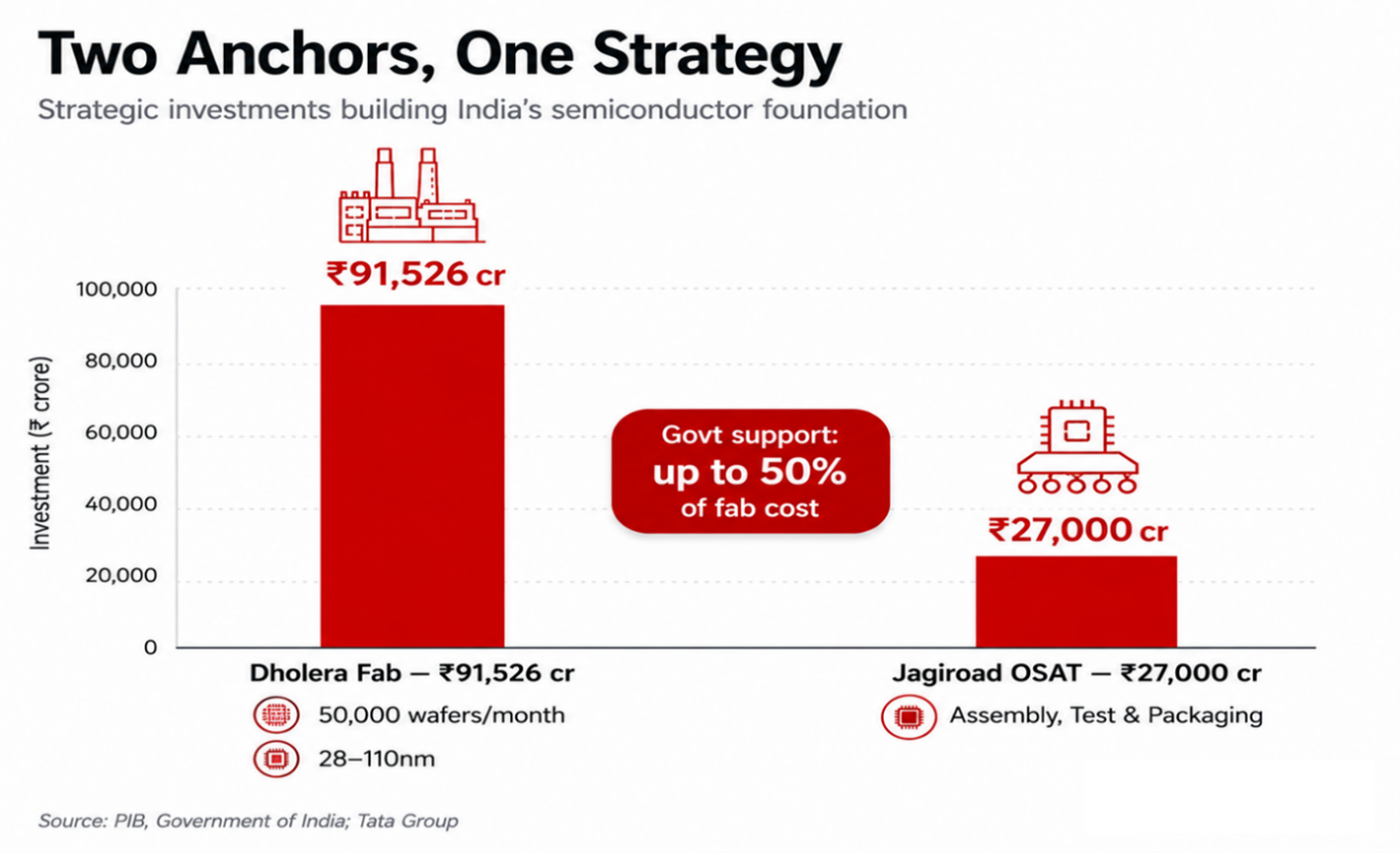

The Dholera Fab (Gujarat)

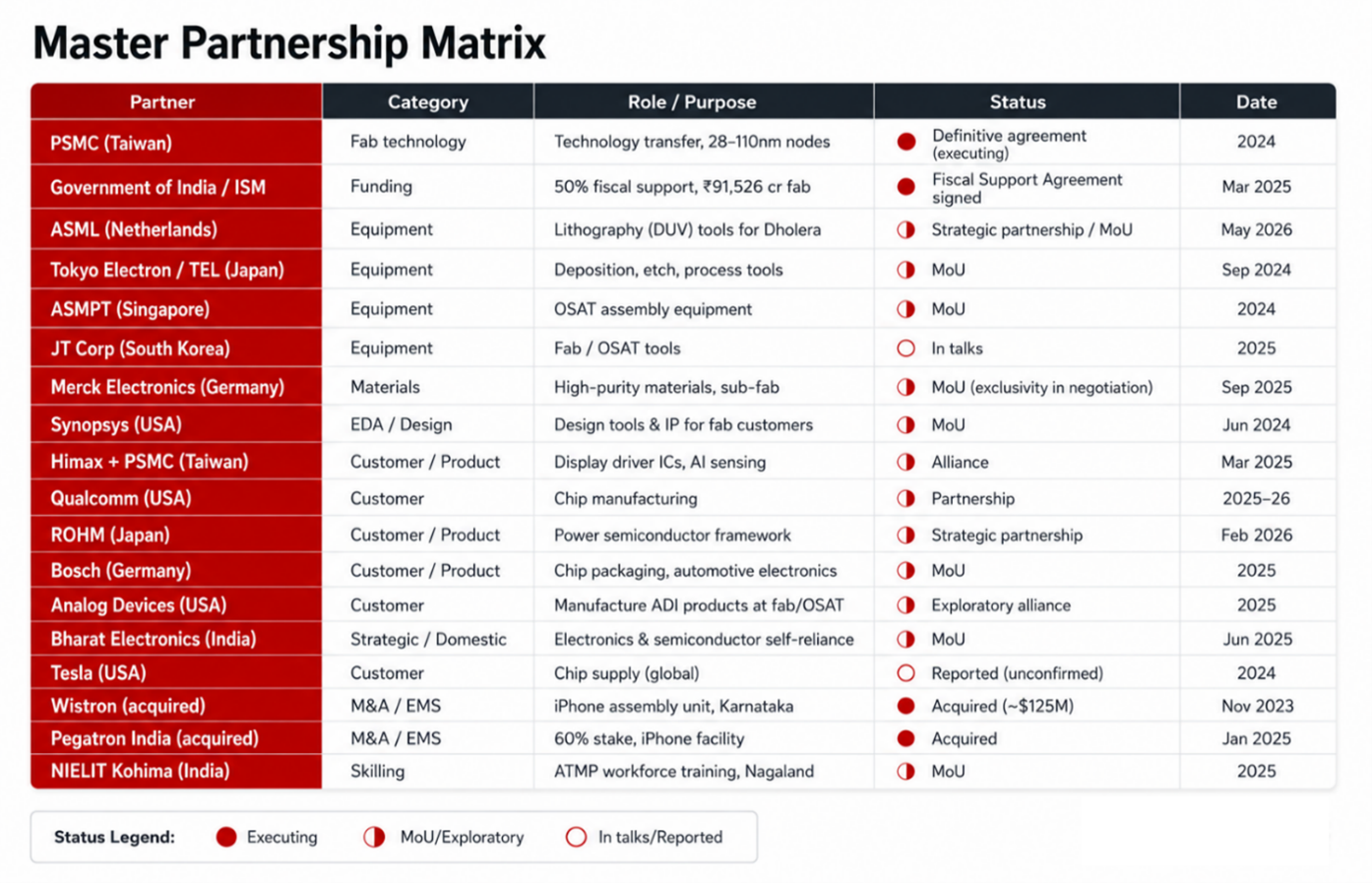

The centrepiece is India’s first commercial wafer fabrication plant in Dholera, Gujarat, built with Taiwan’s Powerchip Semiconductor Manufacturing Corporation (PSMC). The Government of India’s Press Information Bureau confirms a total investment exceeding ₹91,526 crore (around $11 billion) with a planned capacity of 50,000 wafer starts per month, supported by 50% fiscal support from the India Semiconductor Mission on eligible costs [PIB, Government of India]. It is a 300mm (12-inch) fab targeting mature and specialty nodes from 28nm to 110nm, producing power management ICs, display driver ICs, microcontrollers, high-performance computing logic, and automotive chips [EE Times].

The Jagiroad OSAT (Assam)

The second anchor is the greenfield assembly, test, and packaging (OSAT) facility at Jagiroad, Assam, an investment of roughly ₹27,000 crore on a 592-acre former paper-mill site [Tata Group]. Together the two facilities give Tata both halves of the manufacturing chain, front-end wafers and back-end packaging, within India.

The Technology-Transfer Partnership (PSMC)

The single most important enabling relationship is the technology transfer from PSMC, which provides Tata access to a proven portfolio of nodes including 28nm, 40nm, 55nm, 90nm, and 110nm [Tata Group]. This lets Tata bypass the most failure-prone phase of fab development, the years-long struggle to bring a homegrown process to commercial yield. PSMC confirmed the first payment instalment arrived in late 2024, marking execution rather than mere intent [DigiTimes].

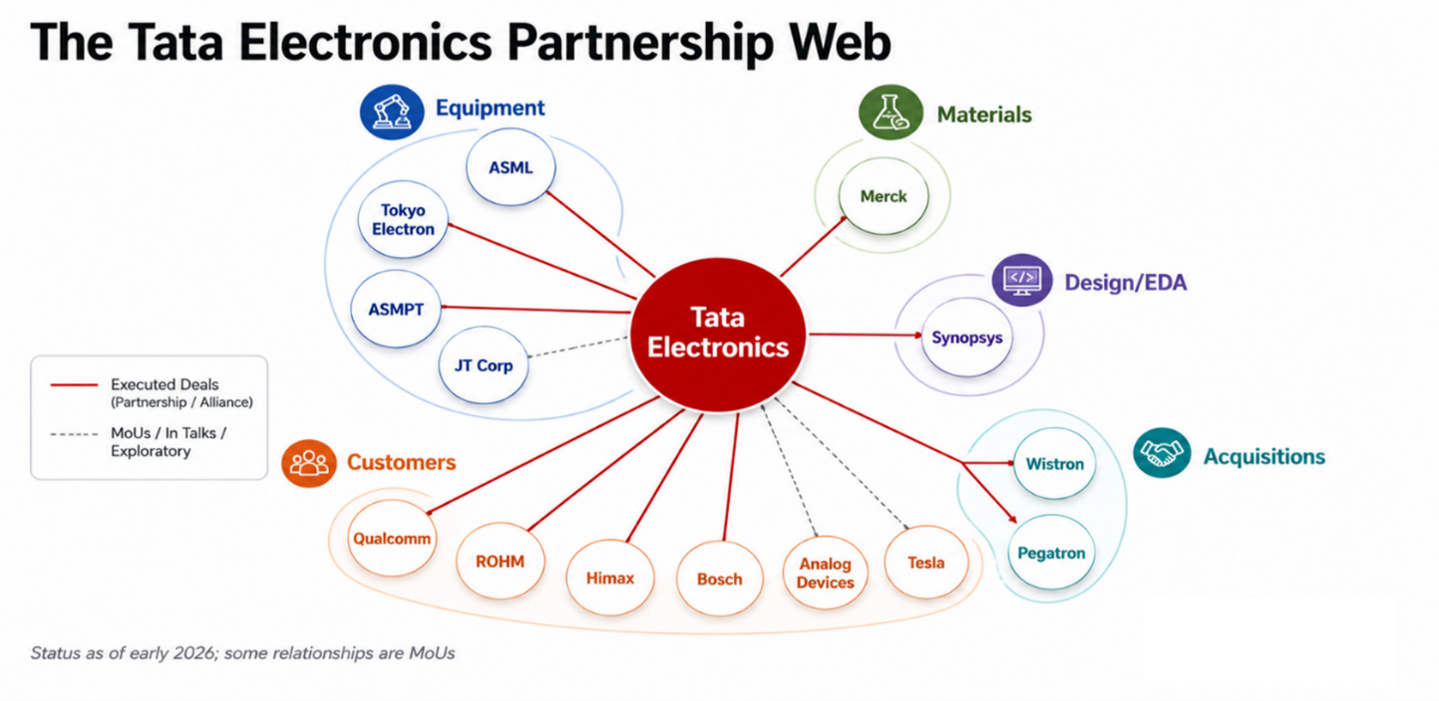

The Equipment Suppliers (the Tool Ecosystem)

A fab is, in effect, a building filled with extraordinarily expensive and specialised tools. Tata has signed partnerships with the world’s leading equipment makers to populate Dholera and Jagiroad.

The most consequential is ASML, the Dutch monopoly supplier of advanced lithography, the machines that print circuit patterns onto wafers. Tata and ASML announced a strategic partnership in May 2026 under which ASML will supply its holistic suite of advanced lithography tools and solutions to enable the establishment and ramp of the Dholera fab [Tata Electronics]. Given Dholera’s 28nm-to-110nm node range, this centres on ASML’s deep-ultraviolet (DUV) systems rather than the bleeding-edge EUV machines, which is appropriate for the targeted nodes [Al Jazeera].

The second pillar tool partner is Tokyo Electron Limited (TEL) of Japan, a leading global supplier of deposition, etch, cleaning, and coating equipment. The two signed a memorandum of understanding in September 2024 to accelerate semiconductor equipment infrastructure for the Dholera fab [Tokyo Electron]. TEL has also been reported to be considering setting up its own operations in India to build local linkages [ET Manufacturing].

For the back-end OSAT, Tata partnered with ASMPT Singapore, signing an MoU to collaborate on establishing semiconductor assembly equipment infrastructure in India [Tata Electronics]. Reporting also placed Tata in talks with additional equipment vendors including South Korea’s JT Corp for the fab and OSAT facilities [ET / LinkedIn]. Industry leaders such as Applied Materials and KLA have also been visible as ecosystem partners around the India Semiconductor Mission and SEMICON India events, signaling the breadth of the tool relationships Tata is cultivating [SEMICON India / Instagram].

The Materials and Chemicals Supply Chain (Merck)

Modern chipmaking consumes vast quantities of ultra-high-purity specialty chemicals, gases, and materials, and securing this supply is as critical as the tools. Tata’s key materials partnership is with Merck Electronics (the German science and technology company), with the two signing an MoU in September 2025 covering safety, manufacturing excellence, semiconductor materials, and sub-fab infrastructure [Tata Electronics]. Reporting indicated Tata was seeking an exclusive long-term supply agreement with Merck for high-purity materials, underscoring how strategically it views the chemicals dependency [DigiTimes].

The Design and EDA Layer (Synopsys)

Before a single wafer is fabricated, chips must be designed, and that requires electronic design automation (EDA) software, an industry dominated by a Cadence-Synopsys duopoly. Tata signed an MoU with Synopsys in June 2024 to accelerate customer product design and ramp for India’s first fab, giving Tata’s prospective fab customers access to silicon-to-systems design tools and IP [Tata Electronics]. This is a quiet but vital piece: a foundry is far more attractive when designers can build for its process using familiar, certified tooling.

The Anchor Customers and Product Alliances

Capacity without committed demand is a path to losses, so Tata has worked hard to lock in customers and co-developed product lines. The most product-specific is the three-way alliance with Himax Technologies and PSMC to develop display driver ICs and ultralow-power AI sensing products, leveraging Himax’s WiseEye AI sensing platform and referencing 28nm and wafer-stacking technologies, effectively giving Dholera an anchor product line [Tata Electronics].

In a major recent development, Qualcomm and Tata Electronics announced a partnership to manufacture chips, a significant validation from one of the world’s largest fabless chip companies [Tata Electronics Newsroom]. In February 2026, ROHM (the Japanese semiconductor maker) formed a strategic partnership with Tata Electronics in the semiconductor business [Tata Electronics Newsroom].

On the automotive and industrial front, Bosch (Germany’s Robert Bosch GmbH) signed an MoU in 2025 to collaborate on chip packaging and manufacturing at Tata’s Assam OSAT and Gujarat foundry, plus automotive electronics [Tata Electronics]. Analog Devices announced a strategic alliance with Tata to explore joint opportunities across India’s semiconductor ecosystem [Analog Devices]. And on the domestic strategic side, Tata signed an MoU with Bharat Electronics Limited in June 2025 to advance India’s self-reliance in electronics and semiconductors [Tata Electronics]. A reported chip-supply arrangement with Tesla for global operations has also circulated, though this rests on press reporting rather than a detailed disclosed contract [ET Now / LinkedIn].

The Acquisitions (Building Downstream Muscle)

Tata’s mergers and acquisitions have centred on the iPhone supply chain, building a large electronics manufacturing services (EMS) base that strengthens its semiconductor ambitions with cash flow, scale, and high-precision manufacturing experience. In November 2023 it acquired Wistron’s iPhone manufacturing unit in Karnataka for around $125 million, becoming the first Indian iPhone assembler. In January 2025 it acquired a controlling 60% stake in Pegatron’s India unit, which operates an iPhone facility [Reuters]. These acquisitions vertically connect Tata’s chip plans to a captive, high-volume downstream electronics business.

The Talent and Skilling Pipeline

A fab and an OSAT require thousands of trained technicians and engineers, a workforce India largely lacks today. Beyond importing senior leadership (CEO Dr Randhir Thakur, former head of Intel Foundry Services [Tata Electronics Leadership]), Tata has begun building the pipeline through skilling MoUs, such as the partnership with NIELIT Kohima to skill the youth of Nagaland for the semiconductor assembly, testing, marking, and packaging (ATMP) sector, relevant to its Northeast India operations [Tata Electronics].

Ongoing and In-Progress Partnerships (Not Yet Finalised)

Several of Tata’s most important relationships are still in active negotiation rather than fully executed, and tracking these “in-flight” deals is essential to understanding the true state of the build-out.

The clearest example sits on the equipment vendor side. As of late 2025, Tata Electronics was reported to be in active talks with multiple global equipment vendors to serve both the Dholera fab and the Jagiroad OSAT, including Dutch lithography maker ASML (since converted into the May 2026 strategic partnership) and South Korea’s JT Corp for the OSAT and fab projects [DigiTimes]. The framing in that reporting, “in talks with multiple potential vendors,” signals that the full tool roster for both facilities is still being assembled rather than locked, which is normal at this construction stage.

On the materials front, the Merck relationship is illustrative of the gap between an MoU and a binding contract. While Tata and Merck signed an MoU in September 2025, reporting indicates the two were still negotiating an exclusive, long-term supply agreement that would make Merck the primary supplier of high-purity materials for the Dholera fab [DigiTimes]. In other words, the strategic intent is set, but the definitive offtake terms were still being finalised.

The ROHM partnership, formed in February 2026, is itself a forward-looking, in-progress collaboration: as an initial focus the two companies aim to establish a manufacturing framework for power semiconductors in India, combining ROHM’s device technology with Tata’s manufacturing, with a stated ambition to expand the lineup of packaged products made in India over time [ROHM]. This is a multi-year build rather than an immediate production deal.

Similarly, the Analog Devices alliance is explicitly exploratory: the two intend to explore opportunities to manufacture ADI’s products at the Gujarat fab and Assam OSAT, language that indicates a framework to be developed rather than committed volume [Tata Electronics]. The Bosch and Bharat Electronics MoUs sit in the same category, signed statements of intent whose concrete manufacturing programmes are still to be defined.

Where Tata is Still Looking for Partners (the Open Gaps)

Reading the ecosystem as a whole, several layers remain only partially filled, and these represent the areas where Tata will likely seek further partners.

The first is the full back-end OSAT tool and bonding ecosystem. While ASMPT is on board for assembly equipment, a complete OSAT requires a wider set of specialists in dicing, wire bonding, advanced packaging, and test handling, and the reported “talks with multiple vendors” suggests this roster is still being completed.

The second is the broad specialty materials, gases, and chemicals supply chain beyond Merck. A single fab consumes a long list of ultra-pure gases, photoresists, slurries, and target materials from many suppliers. Merck addresses high-purity materials, but the wider chemicals and industrial-gases layer (where players such as INOX Air Products operate in the Indian context) appears to still be developing rather than fully contracted [INOX Air Products]. This is a natural area for additional offtake agreements.

The third, and most strategically significant, is advanced-node and future-generation technology. Tata’s current capability tops out at 28nm via the PSMC transfer. There is no announced partner for sub-28nm leading-edge logic, advanced packaging IP such as chiplet and 3D-integration technology, or next-generation processes. If Tata intends to move up the technology curve over time, a future technology partner for advanced nodes is a clear open gap.

A fourth, softer gap is the deepening of anchor demand. Tata has secured marquee names (Qualcomm, Himax, ROHM, Bosch, reportedly Tesla), but a mature-node fab’s economics depend on a deep, diversified customer book. Converting exploratory alliances into firm, high-volume offtake, and adding further fabless and IDM customers, is an ongoing commercial priority rather than a completed task.

Strategic Assessment: How the Pieces Fit

Laid out together, Tata’s ecosystem covers every link of the chain. The PSMC transfer supplies the process; ASML, Tokyo Electron, and ASMPT supply the tools; Merck supplies the materials; Synopsys supplies the design layer; Himax, Qualcomm, ROHM, Bosch, Analog Devices, Bharat Electronics, and reportedly Tesla supply demand and products; the Wistron and Pegatron acquisitions supply downstream scale; and the leadership and skilling partnerships supply talent. Government co-funding of up to 50% materially de-risks the economics.

The candid risks remain real. The strategy is heavily dependent on foreign technology and tool partners in its early phase, which is a sensible bridge but not yet sovereign capability. Mature-node fabs compete in a low-margin, oversupplied global market against subsidised incumbents, so customer commitment and yield ramp will decide profitability. Execution risk on a first-of-its-kind ₹91,000-crore fab without prior high-volume fab experience in the country is significant, and semiconductor timelines routinely slip. Several of the alliances are MoUs (statements of intent) rather than binding contracts, so the gap between announcement and committed volume bears watching.

Conclusion

Tata Electronics is not chasing leading-edge logic supremacy; it is doing something more achievable and arguably more durable, assembling the full industrial stack India has never possessed, and locking in the global tool-makers, material suppliers, designers, and customers needed to make it function. The density and sequencing of its partnerships, from ASML and Tokyo Electron on the equipment side, to Merck on materials, to Qualcomm, ROHM, Himax, and Bosch on the demand side, reveal a company that understands semiconductors are won at the ecosystem level, not the factory level. Whether it reaches anything resembling “supremacy” will be decided by execution over the coming years, but the architecture being built is coherent, comprehensive, and backed by serious capital from both the Tata Group and the Indian state.

If you want a deeper, customised view of India’s semiconductor ecosystem, its players, partnerships, and white spaces, talk to our research team. Get in touch with ExpertLancing ?