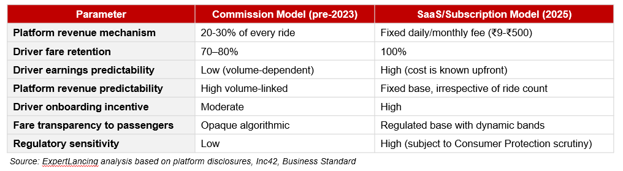

For the better part of a decade, the dominant business model in India’s ride-hailing industry was structurally unchanged: platforms took a 20 to 30% commission on every ride, drivers bore all vehicle costs, and margin pressure was resolved by alternating waves of passenger discounts and driver incentives funded by venture capital. The model worked well at the level of investor narrative. At the level of driver economics, it created chronic dissatisfaction and eventually, a genuine structural challenger.

That challenger arrived not from a well-funded startup or a global mobility giant, but from a collaborative built on open-source infrastructure and a Bengaluru auto-rickshaw drivers’ union. What Namma Yatri, Rapido, and the government’s own cooperative initiative have collectively demonstrated is that the commission model is not just unfair to drivers, it is commercially fragile in a market where drivers have sufficient information, union organisation, and alternative platforms to exit.

The Commission Model and Its Discontents

Auto-rickshaw drivers across Indian cities have long operated at the intersection of high demand and poor earnings. A driver completing 40 rides a day at an average fare of ₹80 generates ₹3,200 in gross receipts. Under a 25% commission structure, the platform takes ₹800, leaving the driver ₹2,400 before fuel, maintenance, and vehicle financing. In cities where CNG prices have risen sharply and traffic congestion compresses daily ride counts, the commission model left little margin.

Driver protests against Ola and Uber became a recurring feature of India’s transport news cycle between 2018 and 2023, particularly in cities like Bengaluru, Hyderabad, and Delhi. Drivers complained not just about commission rates but about opaque algorithmic pricing, cancellation penalties, and the absence of any mechanism to participate in platform decisions. The tension was structural, not episodic, and it set the conditions for a model disruption.

Namma Yatri: Building the Alternative on Open Infrastructure

Launched in November 2022 through a collaboration between payments company Juspay, Nandan Nilekani’s Beckn Protocol foundation, and an auto-rickshaw drivers’ union in Bengaluru, Namma Yatri introduced a structurally different proposition: zero commissions, drivers keep 100% of fares, and the platform charges a nominal subscription fee for technology access. Drivers in most states pay ₹25 per day for unlimited rides, or ₹3.50 per ride for the first ten trips, with no charge beyond that.

The platform was built as open-source infrastructure on the Open Network for Digital Commerce, or ONDC – the government’s open protocol initiative designed to prevent platform monopolies in digital commerce. By positioning itself as mobility infrastructure rather than a closed marketplace, Namma Yatri enabled any ride-hailing operator, city authority, or transport cooperative to build on the same architecture. The company’s founders explicitly compared the model to UPI: “If UPI is the hourglass of payments, Namma Yatri aims to be the hourglass of mobility.”

The market response was faster than most observers expected. By late 2025, the platform had onboarded over 700,000 drivers and facilitated ₹2,000 crore in driver earnings across more than 15 cities, doing so while spending approximately $5 million in total, a stark contrast to the billions burned by Ola and Uber to reach comparable scale. The Economic Survey 2023-24 specifically cited Namma Yatri as an exemplar of India’s open digital infrastructure enabling equitable platform economics.

The Industry-Wide Capitulation

The true measure of Namma Yatri’s impact was not its own market share, it remained relatively small compared to Ola and Uber in absolute rides. Its impact was measured by what it forced its competitors to do. Within two years of Namma Yatri’s launch, every major platform in India’s auto-rickshaw and cab segment had either adopted or announced a transition to subscription-based pricing.

Rapido, which had pioneered a zero-commission subscription model for bike taxis in 2023, extended the same structure to its auto and cab segments. Auto-rickshaw drivers on Rapido pay a dynamic daily login fee of ₹9 to ₹29 and retain 100% of fares thereafter. Cab drivers pay ₹500 per month, but only after their monthly earnings exceed ₹10,000. Following this shift, Rapido reported a 20% increase in driver onboarding, a direct measure of how much the commission model had suppressed participation. In FY24, Rapido posted revenue of ₹648 crore with losses falling 45% year-on-year, demonstrating that the SaaS model can coexist with financial improvement.

Uber moved most consequentially in February 2025, transitioning its Uber Auto product to a zero-commission model with drivers paying a flat daily fee in place of per-ride commissions. Auto ride payments were shifted to cash and UPI only, with Uber explicitly stepping back from being a fare arbitration party to positioning itself as a technology connector. The shift was accompanied by a broader context: Uber’s CEO had noted publicly that Rapido was gaining market share faster than Ola in India’s key markets. Ola followed with a similar zero-commission subscription structure for auto drivers. By mid-2025, the commission-based model that had defined a decade of Indian ride-hailing had been structurally dismantled in the auto-rickshaw segment by three successive waves of competitive pressure – a startup, a domestic scale-up, and an external disruptor.

The Strategic Exhibit: Commission vs. Subscription Model Compared

What It Means for Platform Economics

The subscription model creates a fundamentally different revenue structure for platforms. Rather than earning more when ride volumes are high, platforms earn a fixed, predictable base from every active driver, regardless of how many rides they complete. This lowers revenue upside in high-demand periods but provides resilience during regulatory disruptions, festivals, or weather events that compress ride volumes.

The model also reshapes the competitive dynamic around driver supply rather than passenger discounts. In the commission era, platforms competed by offering higher driver incentive bonuses and passenger subsidies, both funded by investor capital. In the subscription era, platforms compete on the quality of their technology, the reliability of their matching algorithm, and the breadth of their city coverage factors that are harder to replicate through cash.

The risk, noted by industry analysts, is that zero-commission platforms operating on ONDC protocols create a commoditised network where the distinction between Namma Yatri, a new state government cooperative, or a new entrant is minimal. If drivers can access multiple platforms simultaneously at near-zero cost, platform loyalty disappears. This is the same disintermediation risk that ONDC created for e-commerce and India’s mobility ecosystem is beginning to encounter it at speed.

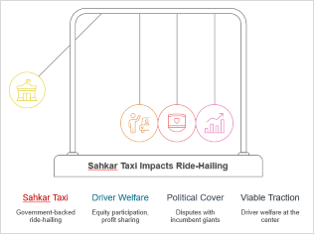

Government Enters as Operator: The Sahkar Taxi Signal

The most structurally significant entrant in this competitive realignment is not a startup but the Government of India itself. Announced in March 2025, Sahkar Taxi is a cooperative-based ride-hailing platform under the “Sahkar Se Samriddhi” (Prosperity through Cooperation) programme. The platform will cover two-wheelers, auto-rickshaws, and four-wheelers, with drivers structured as members of multi-state cooperative societies, entitled to participate in platform governance and share in profits.

Sahkar Taxi addresses the driver-welfare critique of private aggregators at a structural level, not just by removing commissions, but by making drivers equity participants in the platform itself. It also inherits the political cover that a government-backed service carries in disputes with incumbent ride-hailing giants. Several state governments have already experimented with public aggregator models: Kerala’s Kerala Savaari, Goa’s GoaMiles, West Bengal’s Yatri Sathi, and Assam’s Baayu have each demonstrated that government-operated or cooperatively-structured mobility platforms can achieve viable traction when designed with driver welfare at the centre.

Future Outlook: Ecosystem Value Over Ride Revenue

The transition to subscription models is only the first phase of structural change in India’s ride-hailing economy. Platforms that survive the zero-commission era will need to build revenue through adjacent services rather than ride commissions. Rapido’s integration of metro ticketing in Delhi, Chennai, and Hyderabad, Namma Yatri’s multimodal journey planning for the Tamil Nadu government, and Uber’s expansion into corporate travel and teen services all reflect the same strategic direction: monetise the user relationship beyond the ride itself.

For investors evaluating the sector, the implication is clear. A platform’s addressable revenue in India is no longer defined by commission take-rate multiplied by ride volume. It is defined by the breadth of its service ecosystem, the strength of its driver and rider retention, and its ability to integrate into India’s expanding public transit infrastructure as a first-and-last-mile layer. The companies that treat the subscription shift as a revenue model for drivers, rather than merely a response to competitive pressure are the ones building defensible positions for the decade ahead.

Conclusion

India’s transition from a commission-based to a subscription-based ride-hailing economy is one of the most significant structural shifts in the country’s digital services sector in recent years. It was catalysed not by regulation or by global platform strategy, but by a small, open-source startup built from within a drivers’ union. What Namma Yatri demonstrated, and what Rapido, Uber, and Ola have since confirmed through their own model pivots, is that platform loyalty built on asymmetric commission structures was always more fragile than the industry assumed. The next competitive frontier in Indian mobility is not who can take the biggest cut from each ride, it is who can build the ecosystem that drivers and riders genuinely cannot do without.