Food waste is a trillion-dollar liability hiding a multi-billion-dollar ingredient opportunity. Companies that treat waste streams as strategic feedstocks rather than disposal costs are positioned to gain an early advantage as the circular food economy scales.

Key takeaways

- The global upcycled food products market stood at $66.9B in 2025 and is on course to reach $108.5B by 2033, growing at a 6.23% CAGR, propelled by circular economy legislation and tightening food waste regulation.

- New food and beverage launch carrying an upcycling claim grew at a 77% CAGR between 2019 and 2023, outpacing virtually every other sustainability category on the shelf.

- Upcycled Certified snack products grew in 2024 against just 1.4% for the broader food and beverage sector; of consumers say they are more likely to buy a product bearing the upcycled certification seal.

- Four distinct business model archetypes are taking shape, B2B Ingredient Supplier, Branded CPG, Waste-to-Ingredient Platform, and IP Licensing, each with its own margin profile and capital requirement.

- Leading ingredient majors, including Kerry Group, Bunge, AB InBev, and Döhler, are committing capital through direct investments, joint development agreements, and distribution partnerships to lock in proprietary access to upcycled ingredient supply chains.

- The sector has attracted over €7.3B in cumulative funding since 2013, with investment expanding at a 12.9% CAGR from 2019 to 2023

Food Industry Waste: The Scale of the Opportunity

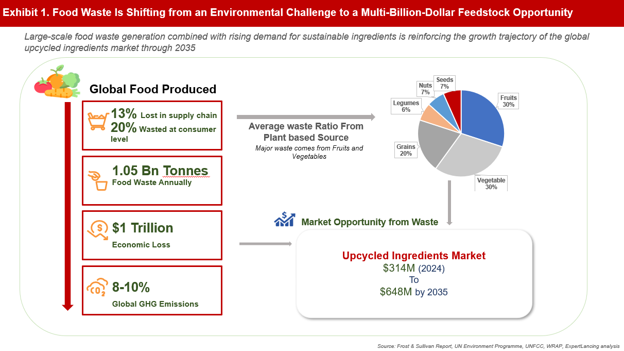

Every year, 1.05 billion tons of food gets lost in the world’s food production system, causing an economic loss of $1 trillion while emitting up to 8 percent to 10 percent of the world’s greenhouse gases in return. One-fifth of food is wasted when it reaches consumers after having been wasted 13 percent along the chain even before hitting the shelves. WRAP forecasts that this cost could escalate past $1.5 trillion dollars by 2030 due to rising demand for food worldwide. (Exhibit 1).

The reason why this is not only an environmental challenge is that the opportunity that is buried under all of this waste is a huge commercial one. Fruits and vegetables constitute the most prominent component of the global food waste category, accounting for more than 50% of all waste produced within various food sectors. In relation to the B2B upcycled ingredients market, the current valuation of $314M will be doubled to $648M until 2035, growing at a CAGR of 6.8%. The wider perspective shows that the ecosystem will grow from $61.7B to $120.2B by 2033.

From Cost Center to Value Driver: Three Forces Reshaping the Economics

Upcycling didn’t make economic sense for most of food industry history. Collection costs were prohibitive, processing technology was half-baked, supply chains couldn’t support it, and consumer willingness to pay for “waste-derived” anything was genuinely uncertain. Three structural shifts have changed that, for good.

- The Technology Is Ready: The economics of production have changed in fundamental ways. Enzymatic hydrolysis, solid-state fermentation, spray-drying, and twin-screw extrusion have all reduced production costs to the point of having practical significance. Planetarians is the perfect example; its use of both solid-state fermentation and twin-screw extrusion allows for the production of textured meat analogs from oil cake proteins, something that wasn’t possible ten years ago. This cost reduction has affected other technologies too, such as cold-press extraction and powder concentration, making fruit-pit oils and spent grain flour economical compared to conventional inputs.

- Certification Built the B2B Trust Layer: Procurement teams don’t buy what they can’t verify. The Upcycled Food Association’s certification program solved that. By 2025, 106 brands and 622 certified SKUs carried the mark, a 17% rise in company participation and ~30% growth in product count year-on-year. Certified participants have collectively diverted over 5.12 million tonnes of food waste since launch. In the natural channel, certified products are growing at +27% in SPINS Natural Enhanced and +39% in certified natural, numbers that give suppliers a concrete basis for premium pricing conversations.

- ESG Has Moved from Marketing to Procurement: The signal for demand is now structural and not reputational. CPGs feel the heat from their investors when it comes to Scope 3 emissions, and upcycled procurement gives you both – real carbon reduction and the verifiable ESG story. Farm-to-Fork by the EU is designed specifically with this in mind. The math from WRAP tells us that there are $14 in savings for every dollar invested in reducing food loss, scaling up to $92 per dollar in the city level.

The next competitive battleground is feedstock access. As demand for circular ingredients accelerates, high-volume waste streams such as brewer’s spent grain, whey, and fruit pomace are becoming strategic raw material assets. Companies securing supply partnerships today are likely to gain lasting advantages in cost, sustainability, and innovation.

Priority Waste Streams: Feedstock Opportunity Concentrates

Commercial attractiveness is determined by four variables working together: volume consistency, biochemical richness, geographic concentration, and how accessible the stream is to processing. The five categories below account for the lion’s share of commercially recoverable ingredient opportunity.

- Brewing- Brewer’s Spent Grain (BSG): BSG is the single largest food-processing byproduct stream by volume, full stop. Global beer production generates roughly 40 million tonnes of BSG annually, yet the vast majority still ends up as low-value cattle feed or in a landfill. That seems almost perverse when you consider what BSG actually contains: 15-26% protein, 40–50% dietary fiber, and meaningful concentrations of ferulic acid and phenolic antioxidants. As raw material streams go, this is one of the most biochemically rich and underutilized at industrial scale.

- Fruit & Vegetable Processing- Pomace, Peels, Press Cake: Fruit and vegetable processing generates byproducts representing 25-30% of raw material weight. Apple and citrus pomace dominate commercial volumes. Utilization rates for citrus pomace in food-grade applications climbed 12% year-over-year in 2024. Cold-pressed oils and aqueous extracts from berry and grape seeds are rich in antioxidants and essential fatty acids; by 2025, demand for these liquid fractions in premium skincare formulations had grown 15%, as brands hunted for natural, upcycled ingredients to reach eco-conscious consumers.

- Dairy- Cheese Whey: Global whey production runs at roughly 180- 200 million tonnes per year. The real opportunity, though, lies one step further: extracting bioactive peptides for nutraceutical and clinical nutrition markets, where value-per-unit jumps by an order of magnitude over commodity WPI.

- Aquaculture & Fisheries- Processing Residues: Fish processing generates frames, skins, heads, and viscera that can represent 20-80% of total fish weight, depending on species and processing method. Omega-3 concentrates derived from aquaculture byproducts represent a multi-billion-dollar whitespace with limited incumbent competition, particularly at pharmaceutical-grade purity levels.

- Oilseed & Grain Processing- Press Cakes and Bran Fractions: Sunflower, rapeseed, and hemp press cakes contain 30-45% protein by dry weight. As plant-based protein markets tighten on the supply side, these press cakes are emerging as cost-advantaged alternative feedstocks. Grain milling, meanwhile, generates bran fractions rich in arabinoxylan dietary fibers, prebiotic substrates currently priced like commodity byproducts, despite their genuine functional food potential.

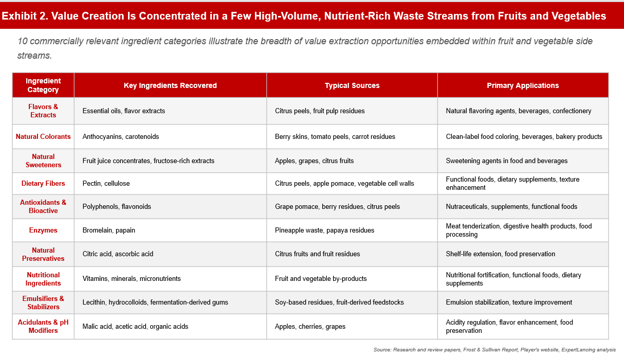

In the case of prioritized feedstocks for food-waste valorization, the use of residues from fruits and vegetables is notable due to the range of ingredients that may be extracted from the one particular waste product. This includes fibres, antioxidants, pigments, organic acids, and bioactive compounds, which may then be used to produce ingredients for various uses in the food, beverage, nutraceuticals, and cosmetics industries. With advancements in extraction methods and increasing market demands for cleaner ingredients, such residues are being increasingly recognized as strategic feedstocks. (Exhibit 2).

Emerging Technology: Platforms Unlocking Waste Value

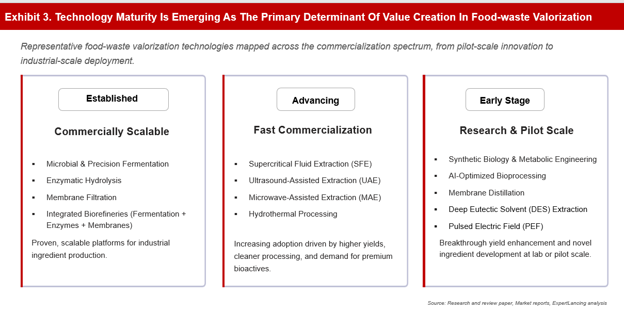

Technologies will enable scaling of upcycled ingredient manufacturing. Known technologies like fermentation, enzyme technology, and membrane filtration have already started enabling upcycling of ingredients on a larger scale, while advanced technologies like advanced extraction are making it possible to get high-value bioactive or functional ingredients from waste material. In future, AI-powered biotechnology and biorefineries are likely to enhance ingredient functionalities. (Exhibit 3)

Among established platforms, microbial fermentation and precision fermentation, enzymatic hydrolysis, and membrane filtration have gained prominence as the most scalable approaches for turning side streams like spent grains, whey, and pomace into protein, fiber, bioactive, and functional ingredients. These approaches are being increasingly adopted due to their economic feasibility and suitability for manufacturing processes.

A second set of technologies is advancing towards commercialization at a fast pace. Supercritical Fluid Extraction, Ultrasound-assisted Extraction, Microwave-assisted Extraction, and Hydrothermal Processing are some of the key ones that have gained prominence owing to their ability to enhance yield of extraction process, minimize the use of solvents, and facilitate clean label ingredients. The applications include recovery of valuable chemicals like polyphenols, antioxidants, dietary fiber, carotenoids, and omega-3 fatty acids.

Other than the above-mentioned technologies, there is still a number of emerging technologies that, while currently at the experimental stage, have much promise in the future. These include synthetic biology and metabolic engineering, optimized bioprocessing via artificial intelligence, membrane distillation, DES extraction, PEF technology, and biorefineries integrating processes like fermentation, enzymatic conversion, and membrane separation. All these technologies are anticipated to increase efficiency of the production processes and improve the quality of food waste-derived compounds and ingredients (Exhibit 3).

Key Innovators: Shaping the Upcycled Ingredients Market

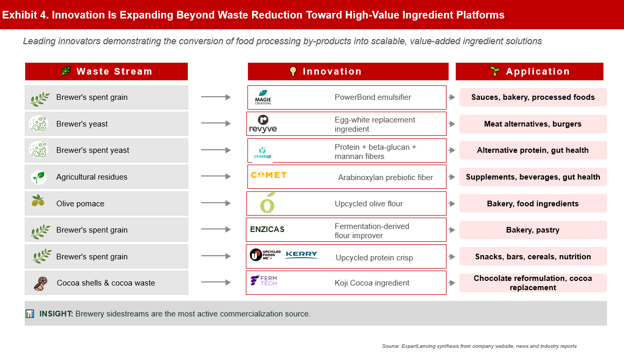

The competitive landscape is evolving around three models: feedstock owners, ingredient innovators, and branded product companies. While specialized startups continue to drive innovation, major ingredient suppliers are increasingly entering the space through partnerships and investments. Success will depend on securing feedstock access, scaling processing capabilities, and developing differentiated ingredient portfolios (Exhibit 4).

Companies are increasingly prioritizing waste streams that offer both nutritional functionality and scalable supply, enabling the transition from waste management to high-value ingredient production. Among these, brewer’s spent grain and spent yeast have emerged as the most commercialized feedstocks, reflecting their consistent availability, protein and fiber richness, and suitability for a wide range of food and nutrition applications. Major ingredient suppliers such as Cargill, Ingredion, Roquette, Kerry Ingredients, DSM-Firmenich, and Givaudan are increasingly participating alongside specialized upcycling innovators including ReGrained, Renewal Mill, BLUE STRIPES, and Upcycled Food, Inc. While Exhibit 4 highlights representative participants, the market remains highly fragmented, with more than 100 companies globally developing upcycled ingredients across diverse waste streams and application areas.

Whitespace Opportunities: Future Growth Vectors

With the completion of the industry’s pivot from a focus on reducing waste toward one of creating value, the next phase of expansion will stem from premium applications, regional processing hubs, and the digital infrastructure supporting these processes.

Functional & Nutraceutical Applications: The use of bioactives from food waste for the production of pharmaceuticals and nutraceuticals represents the most valuable use case currently supported by upcycling technology. There have been promising results in the use of olive leaf extract, citrus peel polyphenols, and spent brewer’s yeast as sources of antioxidants, anti-inflammatories, and antimicrobials. Firms that possess both processing infrastructure and nutraceutical connections are well positioned to take advantage of such opportunities.

Upcycled Pet Food: Pet products emerged as the number one Upcycled Certified category in 2025, overtaking snacks and beverages. Pet food consumers show strong willingness to pay for traceable, sustainable ingredients, and the regulatory environment is more permissive than for human food, which makes it an attractive entry vector for brands looking to prove the model before expanding to human food markets.

Asia-Pacific Industrialization: Asia-Pacific is positioned as the fastest-growing upcycled ingredients market in the world, driven by India’s 2026 Food Loss Reduction Roadmap and China’s wet-market separation pilots running across 36 mega-cities. First-mover infrastructure investments, particularly in fermentation capacity and cold-chain-enabled ingredient processing, will be very difficult to replicate once regional champions emerge and lock in supply relationships.

B2B SaaS & Traceability Platforms: The certification and provenance verification ecosystem is an underserved infrastructure layer with its own commercial logic. The acquisition of the Upcycled Certified program by a publicly traded verification companies a signal: trust infrastructure has standalone value, entirely independent of ingredient production. That is a meaningful whitespace for platforms, not just ingredient makers.