India’s shared mobility story has, for the most part, been told through the lens of its largest metros. Bengaluru gave Rapido its first market, Ola built its early user base in Mumbai and Delhi, Yulu’s electric bikesharing found its first institutional traction in Mumbai and Hyderabad, and Cityflo proved the demand-responsive shuttle concept in the financial district corridors of Bandra-Kurla Complex. Metro cities provided the density, digital infrastructure, and venture capital ecosystem that enabled the industry’s early scaling.

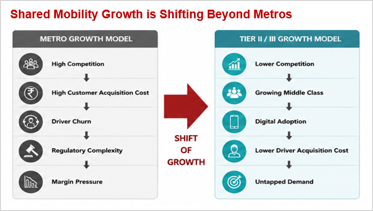

After more than a decade of expansion, the industry’s growth equation is beginning to change. Metro markets remain strategically important, but intense competition, rising customer acquisition costs, regulatory uncertainty, and pressure on driver economics are making incremental growth increasingly difficult. The next wave of expansion is likely to emerge from India’s hundreds of mid-sized cities, where organised shared mobility remains limited despite rising incomes, growing digital adoption, and increasing travel demand. Rather than representing a gap in service, these cities represent the industry’s largest untapped growth opportunity.

The Structural Case: India’s Urban Mobility at a Tipping Point

At first glance, India’s relatively low level of vehicle ownership appears to suggest that personal mobility remains underdeveloped. In reality, the country’s urban transport system faces the opposite challenge. Rapid growth in vehicle ownership is placing increasing pressure on road infrastructure that has expanded far more slowly than travel demand. As congestion intensifies and parking becomes more constrained, cities are reaching a point where adding more privately owned vehicles is becoming progressively less efficient. Shared mobility therefore represents not only a sustainable transport option but also a more efficient way to utilise existing urban infrastructure.

The imbalance between vehicle growth and transport infrastructure further reinforces this challenge. While private vehicle ownership has continued to expand steadily over the past decade, investment in urban road capacity has not kept pace. The resulting congestion increases travel times, raises operating costs, and limits the efficiency of conventional commuting patterns. Higher vehicle utilisation through shared mobility offers one practical way of improving transport efficiency without requiring proportional expansion of physical infrastructure.

What is changing now is the geography of this demand. The Indian middle class, currently estimated at 38% of the total population and projected to reach 60% by 2047, is expanding fastest in Tier II and III cities. Rising aspirational incomes in cities like Vijayawada, Coimbatore, Nagpur, Bhopal, and Raipur are generating the same mobility demand that Bengaluru and Pune exhibited five years ago, but without the public transit alternatives that metro residents, however inadequately, can access.

The 437-City Gap in Context

India has 437 cities with populations above 100,000. Organised, app-based shared mobility is meaningfully present in fewer than 120 of them. That gap represents a user base of hundreds of millions of potential commuters with the smartphone penetration, UPI familiarity, and income levels to support formal shared mobility, but with no credible service offering competing with private vehicle ownership.

The access asymmetry is visible across segments. Ridehailing, the most mature of India’s shared mobility categories, has its fleet concentrated in the top 30 to 40 cities. Bikesharing, which could serve the short-distance commuting needs of Tier II cities most effectively, has fewer than 70,000 active vehicles across the country as of 2024. Demand-Responsive Transit shuttles, the fastest-growing segment, with a projected revenue CAGR of 41.4% through 2035, operate almost entirely in metro and large Tier I markets, because most operators have focused on corporate commuter corridors where ticket sizes are higher and route density is predictable.

Rapido’s expansion from 120 to 500 cities is the clearest signal that the industry has begun to recognise this geography. In markets like Bhopal, Nagpur, and Vijayawada, Rapido already operates more daily rides than Ola in the same city, demonstrating that Tier II demand is real and that a lean, two-wheeler-first approach can achieve market leadership faster than the four-wheeler-heavy playbooks that defined metro expansion.

The Electrification Enabler

The economic case for Tier II and III expansion is meaningfully improved by electric vehicles. In metro cities, EV adoption in shared fleets has been constrained by charging infrastructure gaps, range anxiety for longer inter-city routes, and the upfront cost differential relative to ICE vehicles. In Tier II cities, shared mobility use cases are predominantly short-distance intra-city trips, precisely the use case where EV economics are strongest.

The government’s PM e-Drive scheme provides a subsidy of ₹58/kWh for two-wheelers, capped at ₹117, alongside registration and road tax waivers. The FAME II programme had already set the foundation; PM e-Drive replaces and expands it with targeted subsidies for passenger three-wheelers and two-wheelers used in commercial fleets. For a Tier II city operator deploying 500 electric scooters for a shared service, these subsidies meaningfully reduce the capital outlay that has historically made fleet deployment in smaller markets uneconomic.

The national target for electric two-wheelers is 70 to 80% of new sales by 2030. Shared fleet deployments in Tier II cities where vehicles are used 6 to 10 times more intensively than private cars offer the highest emissions reduction per vehicle electrified. This alignment between fleet electrification economics and national sustainability goals creates a window for operators, OEMs, and state governments to co-invest in Tier II shared electric mobility at scale.

Operator Strategies for Smaller City Entry

The business model required for Tier II and III cities differs meaningfully from the metro playbook. In metros, shared mobility platforms competed primarily on app quality, pricing, and driver supply density. In smaller cities, the primary barriers are different: informal transport networks (predominantly shared autos and private buses running fixed routes), lower digital literacy among potential drivers, cash-heavy payment preferences, and the absence of the regulatory and infrastructure support that smart city investments have provided to larger urban areas.

Successful Tier II entry requires hyperlocal design, smaller initial fleet commitments with high utilisation rather than wide geographic coverage, partnerships with existing informal transport operators rather than attempts to displace them, and revenue models that acknowledge lower average ticket sizes. The operator strategies documented in Frost & Sullivan’s 2025 analysis of India’s shared mobility landscape align with this logic: positioning carsharing as an alternative to ownership in college towns and corporate hubs, digitising existing informal rickshaw networks rather than building new ones, and designing bikesharing deployments around specific high-density corridors – bus stands, colleges, and markets, rather than attempting city-wide coverage.

The government’s Smart Cities Mission, which has allocated significant capital to 100 designated cities for urban infrastructure development, provides an institutional entry point that operators have used effectively. Mybyk’s partnership with Smart City Ahmedabad Development Limited for dockless bicycle-sharing, Yulu’s metro station deployments in Delhi and Bengaluru, and CRUT Bhubaneswar’s public e-rickshaw programme for first-and-last-mile connectivity all demonstrate that government partnerships are a viable and cost-efficient distribution channel in smaller cities.

The Investment Thesis

For venture capital and growth equity investors who have been cautious about India’s shared mobility sector because of thin unit economics in metro markets, the Tier II and III opportunity represents a structurally different risk profile. Competition is lower, driver acquisition costs are lower, and the regulatory environment while inconsistent, is less adversarial than in metros where incumbent transport unions wield political influence.

The fastest-growing segment in this geography is Demand-Responsive Transit, driven by B2B corporate commuter demand. Cityflo, which has announced plans to operate 500 buses across five metro cities by 2026, provides a template that translates directly to Tier II markets with large industrial clusters and special economic zones. Cities like Pune, Surat, Rajkot, and Coimbatore have significant concentrations of manufacturing and IT employees who currently rely on private vehicles for commutes because no reliable organised shuttle service exists. The addressable market in these corridors is in the hundreds of millions of dollars annually.

Related Reading: Multimodal Integration as the Long-Term Architecture

The Tier II mobility expansion will be most durable when it connects to, rather than competes with, India’s expanding public transit network. Metro rail networks are being built in 27 cities beyond the established systems in Delhi, Mumbai, and Bengaluru, according to the Ministry of Housing and Urban Affairs. Shared mobility, particularly last-mile electric bike taxis and auto-rickshaws becomes structurally essential rather than discretionary when a metro station opens in a city where 70% of potential users cannot easily access it from their homes.

Conclusion

India’s shared mobility sector is at a strategic inflection point. Metro markets have provided proof of concept for every segment, ridehailing, bikesharing, bike taxis, DRT, and carsharing, but are approaching a ceiling defined by competitive density, regulatory complexity, and infrastructure saturation. The next phase of growth will be built not in Bengaluru or Mumbai, but in the 400-plus cities where rising incomes are creating transport demand, private vehicle ownership is straining infrastructure, and organised shared mobility is nearly absent. For operators who can adapt their business models to this geography leaner, more local, EV-first, and government-partnered the opportunity is both commercially substantial and structurally defensible. The 437-city gap is not just an underserved market. It is where India’s shared mobility industry will be defined.