A global semiconductor manufacturer with a strong portfolio of analog, logic, power discrete, and sensor products wanted to understand where its next growth opportunities would come from in emerging markets across Asia Pacific, the Middle East and Africa, and Latin America. The company was operating in an increasingly competitive environment, facing pressure from regional manufacturers, supply chain disruptions driven by geopolitical events, and a decline in revenue from its industrial systems business during 2024.

To support future growth, a detailed market assessment was carried out with forecasts through 2029. The study highlighted the most attractive opportunities by identifying railways, AI-based testing, and EV charging infrastructure as the fastest-growing application areas. It also provided an in-depth analysis of more than 60 competitors across 12 product categories and evaluated the market potential of key emerging economies. Based on these insights, a phased market entry strategy was developed for five priority countries, helping the client focus its R&D investments and expansion efforts on the markets with the strongest long-term growth potential.

The Challenge

The global industrial semiconductor market was valued at around USD 48 billion in 2025 and is expected to reach nearly USD 97 billion by 2035, growing at a CAGR of 7.4%. While the market outlook was positive, the real challenge was identifying where the strongest growth opportunities would emerge. The industrial semiconductor landscape covers more than 50 end-use applications, each with different demand patterns, technology requirements, regulatory standards, and competitive intensity. For a company serving industries such as industrial automation, energy, aerospace and defense, and medical devices, deciding where to invest limited R&D budgets, sales resources, and channel partnerships was becoming increasingly complex, especially across fast-growing emerging markets.

The client wanted clear answers to three key business questions. First, which industry verticals in emerging markets were likely to recover the fastest and deliver the highest growth through 2029? Second, which compound semiconductor technologies, including silicon carbide (SiC), gallium nitride (GaN), and indium phosphide (InP), should be prioritized in the product roadmap for different applications? Third, what was the most effective route to market in each region, whether through direct sales, distributor partnerships, or value-added resellers? Answering these questions was essential for building a focused growth strategy and ensuring that investments were directed toward the markets and technologies with the highest long-term potential.

The Approach

The engagement was structured in four distinct phases over a 14-week period.

Phase 1: Market Landscape and Baseline Sizing. The team conducted secondary research across industry databases, trade publications, patent filings, and government investment announcements for the five end-user verticals, five product categories (analog, logic, memory, discrete, and optical/sensors), and three emerging-market regions. Revenue forecasts were built through 2029 using a bottom-up methodology tied to end-device unit sales, semiconductor content per device, and average selling price trajectories.

Phase 2: Competitive and Ecosystem Mapping. The analysis profiled more than 60 competitors across APAC, MEA, and Latin America, ranging from global leaders such as Texas Instruments, Analog Devices, Infineon, and STMicroelectronics to regional challengers including BYD Semiconductor, Sanan IC, and Leapers Semiconductor. Distribution channel economics were benchmarked: 52.5% of 2024 revenues flowed through distributors, while 47.5% came via direct sales. Seven notable M&A transactions between 2021 and 2024 were analyzed for strategic pattern recognition, including Renesas’s acquisition of Transphorm, Infineon’s absorption of GaN Systems, and Onsemi’s purchase of GT Advanced Technologies.

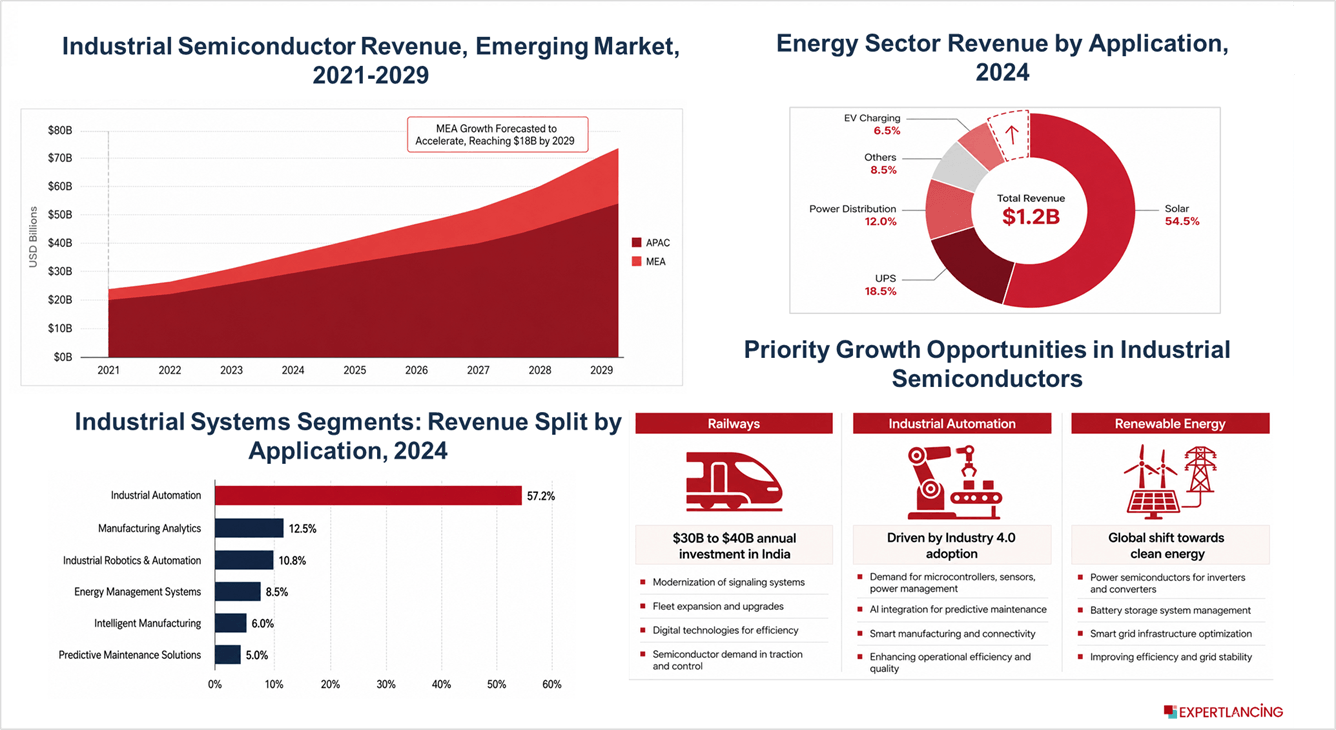

Phase 3: Vertical Deep Dives and Growth Opportunity Scoring. Each vertical (industrial systems, energy, aerospace and defense, medical, and a composite “others” category covering railways, test and measurement, building automation, and smart water) was analyzed for semiconductor demand drivers, restraint factors, technology adoption curves, and compound semiconductor penetration potential. Three verticals were identified as priority growth opportunities based on a weighted scoring model combining market size, CAGR, semiconductor content uplift potential, and policy tailwinds.

Phase 4: Regional Go-to-Market Blueprint. For each priority vertical, the team developed a region-specific entry and expansion playbook. This included recommended distribution models, partner shortlists, regulatory considerations, and a phased investment timeline aligned with government infrastructure spending cycles, particularly India’s $30 billion to $40 billion annual railway investment and the broader APAC push toward 30% EV penetration by 2030.

Key Findings and Insights

The analysis revealed that the APAC emerging-market region would grow at an 8.9% CAGR from 2024 to 2029, reaching $42.23 billion by the end of the forecast period, outpacing the MEA region’s 7.4% CAGR. Within APAC, India emerged as the single largest opportunity node, supported by 10 approved semiconductor projects representing approximately $19 billion in committed investment and a Union Budget 2026 that allocated the largest-ever outlay for Indian Railways, including seven new high-speed rail corridors.

A critical finding challenged the client’s existing portfolio emphasis. While industrial automation represented 57.2% of the industrial systems segment and remained the largest revenue contributor, its recovery trajectory was slower than three smaller but faster-growing verticals. Railways, projected to grow at above-market-average rates, offered immediate scale through India’s $30 billion to $40 billion annual conventional rail investment plus an additional $10 billion to $20 billion in metro projects. EV charging, though contributing only 3.7% of the energy segment’s 2024 revenue, stood at an inflection point as the global EV charging infrastructure market was projected to grow at 18.5% CAGR through 2035. AI-assisted testing, driven by the integration of ML-based automatic test pattern generation and GenAI-powered test program creation, was positioned to increase semiconductor content per tester unit by embedding AI-ASICs and accelerators.

Counter to prevailing assumptions, the study found that Western reshoring strategies were less relevant to the client’s growth agenda than friend-shoring into cost-competitive emerging economies. Establishing back-end fabrication for power semiconductors in select APAC and Latin American markets could deliver cost advantages that pure reshoring to North America or Europe could not match.

The compound semiconductor opportunity proved larger than the client had anticipated. The global SiC and GaN power semiconductor market, valued at $4.1 billion in 2025, is projected to reach $38.9 billion by 2035 at a 25.3% CAGR. Within the client’s addressable verticals, SiC demand was concentrated in solar PV inverters (where semiconductor content represented 20% to 40% of total inverter cost), EV charging DC fast-charging stations, and railway fleet electrification requiring high-voltage power products.

The Impact

- 9% CAGR Growth Pathway Quantified.The engagement produced a granular five-year revenue forecast across three regions, five verticals, and five product categories, giving the client a defensible investment case for board-level resource allocation.

- Three Priority Verticals Identified and Ranked.Railways, EV charging, and AI-assisted testing were validated as above-market-average growth opportunities, collectively representing a serviceable addressable market exceeding $15 billion by 2029 across emerging economies.

- 60+ Competitor Profiles Delivered.A competitive intelligence database covering market positioning, product portfolios, M&A activity, and distribution strategies across APAC, MEA, and Latin America was handed off to the client’s regional strategy teams.

Strategic Takeaway

The industrial semiconductor market’s fragmentation is both its greatest complexity and its greatest source of hidden growth. Companies that invest in granular, vertical-specific market intelligence across emerging economies, rather than relying on aggregate global forecasts, will identify asymmetric growth windows that competitors miss. As sustainability mandates, AI convergence, and infrastructure modernization reshape demand across railways, EV charging, and industrial testing, the firms that act on precision intelligence today will define the competitive landscape of 2030.

Ready to Map Your Next Growth Frontier?

If your organization is navigating emerging-market entry, vertical prioritization, or compound semiconductor strategy in the industrial sector, we can design a tailored intelligence engagement. Contact us to start the conversation.