The 2026 Iran conflict has triggered a major petrochemical feedstock disruption across methanol, ethylene, LPG, naphtha, and polymer supply chains. The disruption is forcing producers, buyers, and investors to reassess global petrochemical feedstock supply across methanol, ethylene, LPG, naphtha, and polymer chains.

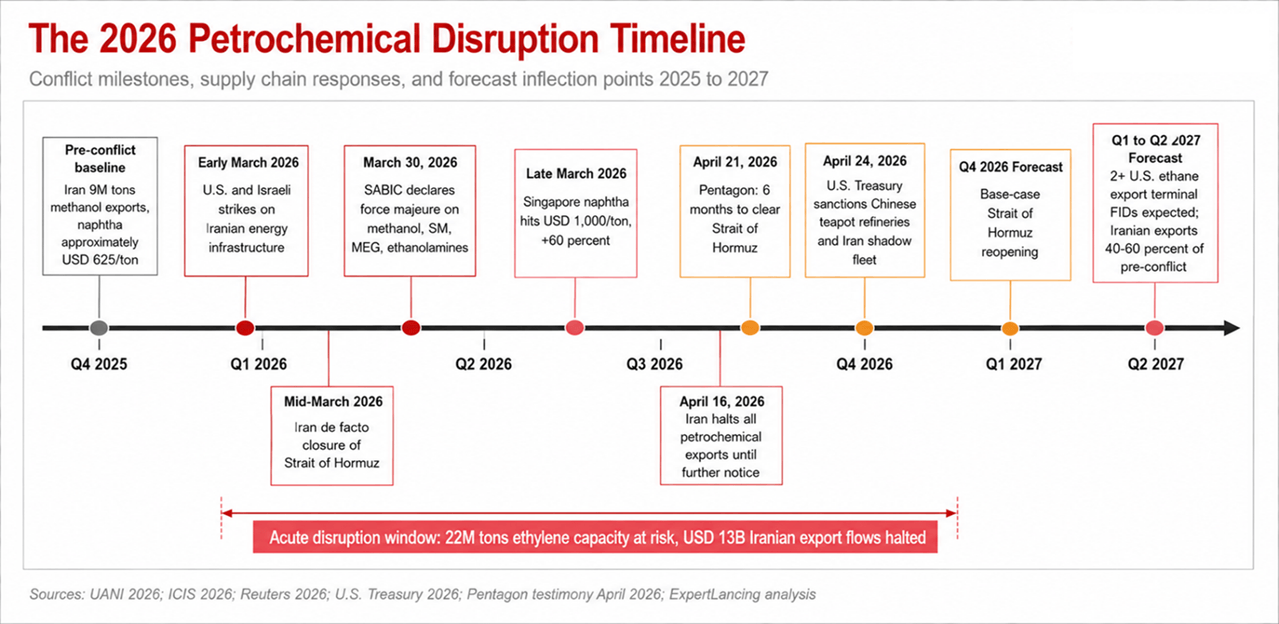

The Iran conflict that escalated in early March 2026, following U.S. and Israeli strikes on Iranian energy and petrochemical infrastructure, has produced the largest disruption to global petrochemical feedstock flows since the 1973 oil shock. Iran’s mid-March de facto closure of the Strait of Hormuz, documented by United Against Nuclear Iran’s tanker tracker and corroborated by Pentagon testimony to the U.S. House Armed Services Committee on April 21 (which estimated six months to fully clear the strait), has severed the artery through which roughly 20 percent of global crude oil and a comparable share of LPG, naphtha, methanol, and ethylene moves to market, according to ICIS analysis published March 4. This makes the Strait of Hormuz petrochemical supply corridor central to both methanol and ethylene supply disruption.

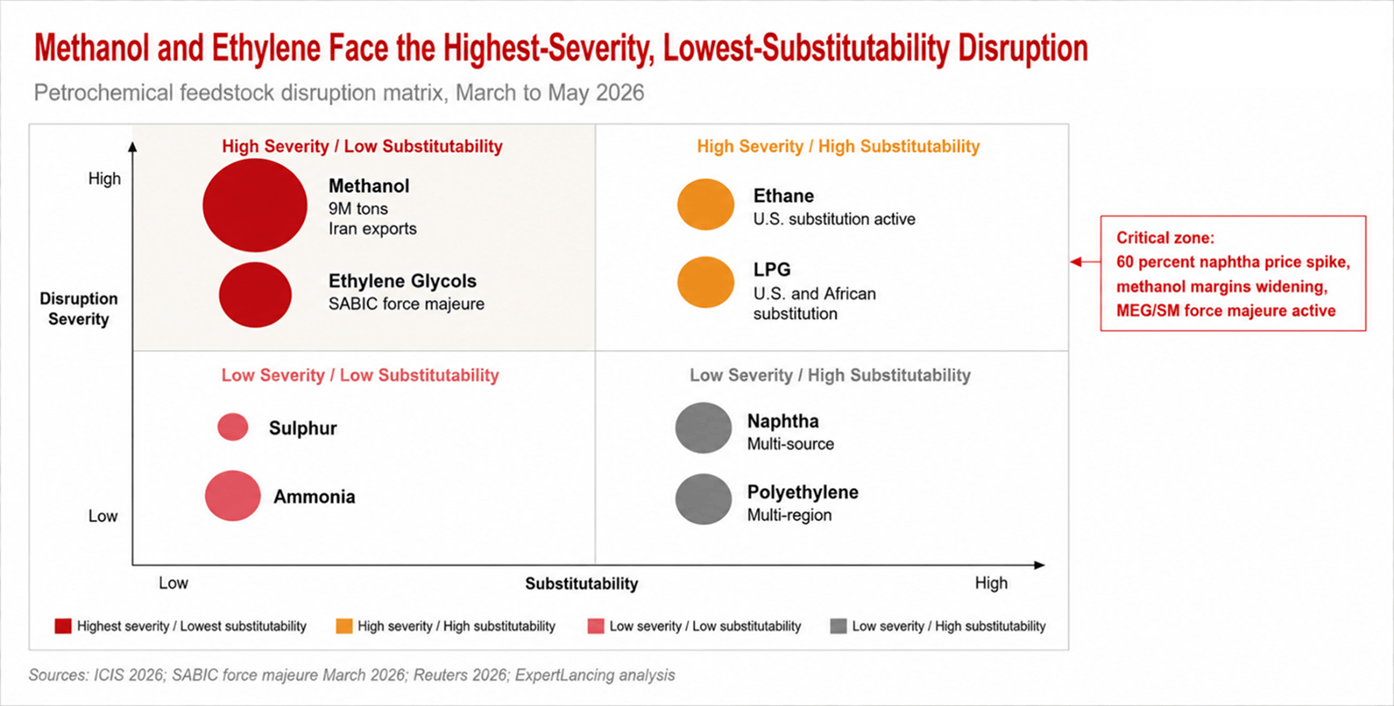

The headline price moves tell part of the story. Singapore naphtha touched USD 1,000 per ton in late March, a 60 percent jump from pre-conflict levels per Coface and Financial Content reporting. Methanol producer margins widened sharply as Iranian supply, roughly 9 million tons exported in 2025, was abruptly removed. Chemdo and SunSirs forecast global ethylene production could fall by more than 22 million tons in 2026 against a 2025 base of 185 million tons. Saudi Aramco declared force majeure on Asian shipments through March 31, and SABIC followed with a force majeure on methanol, styrene monomer, ethylene glycols, and ethanolamines. Sadara and SABIC combined have removed approximately 1.5 million tons per year of ethylene capacity from accessible global markets.

The contrarian view we hold is this: the price spike is the visible crisis, but the durable consequence is a structural rewiring of feedstock flows that will not reverse even after the strait reopens. The 2026 shock has accelerated a U.S. ethane and LPG export build-out, a Chinese feedstock substitution strategy, and a European naphtha demand destruction cycle that together will permanently shift where the 2030 petrochemical industry sits. Decision makers who treat this as a transitory event will lose. Those who treat it as a structural reset will define the next decade.

The Feedstock Map Before the Conflict

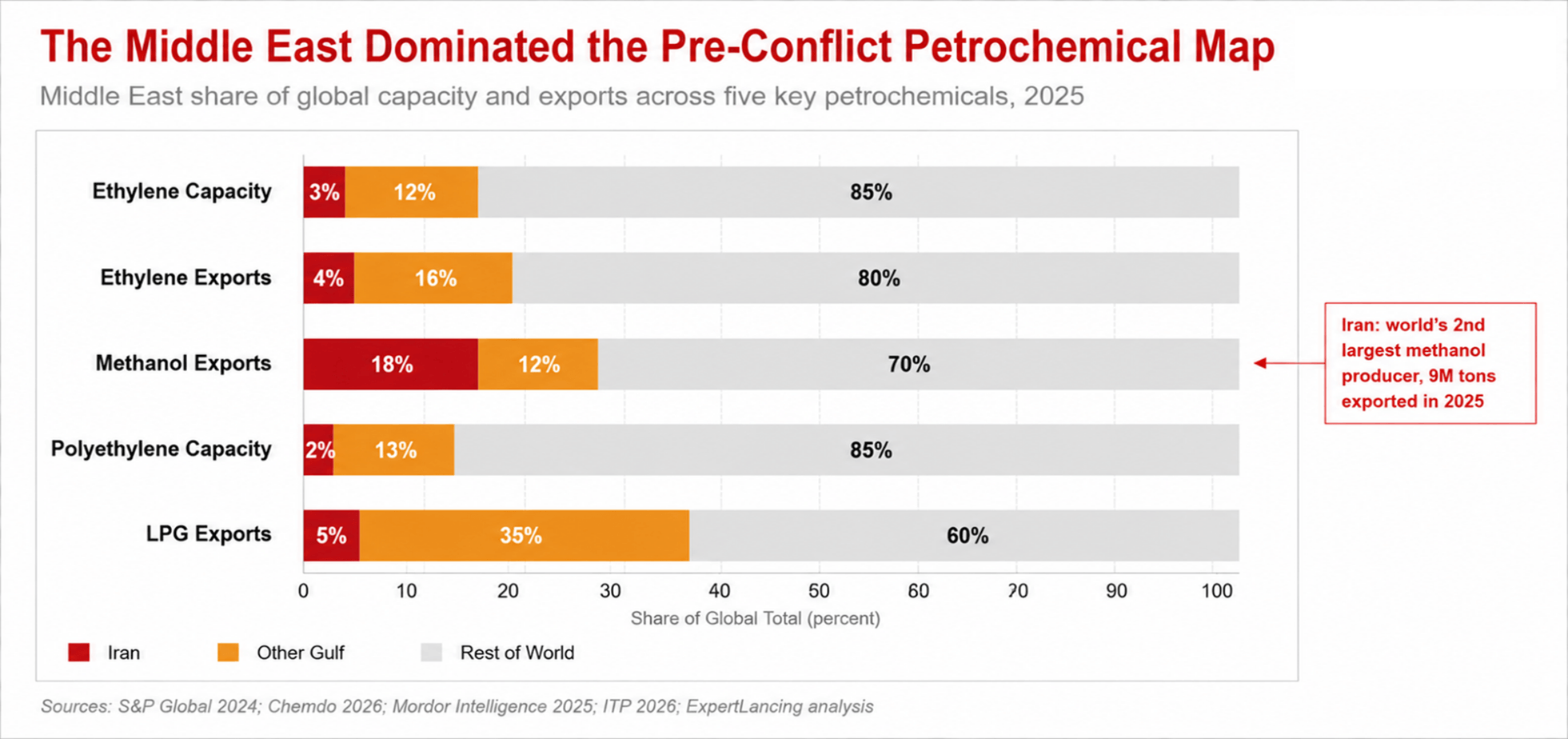

Before March 2026, the Middle East accounted for approximately 35 million tons of ethylene capacity (roughly 15 percent of the global 232 million ton base per Chemdo), 20 percent of global ethylene export volume, and a dominant share of methanol export trade. Iran alone produced approximately 10 million tons of methanol, 7 million tons of ethylene, 8 million tons of urea, and 5 million tons of polyethylene in the 2024 to 2025 fiscal year. China, the world’s largest methanol importer at 14.4 million tons in 2025 (roughly 13.5 percent of its total domestic methanol consumption), sourced approximately 58-59 percent of those imports from Iran by actual origin, equivalent to roughly 8 million tons and under 8 percent of total Chinese methanol consumption with total Iranian methanol exports to China exceeding 5 million tons in 2024.

Saudi Arabia held 39.35 percent of the Middle East polyethylene market in 2025 per Mordor Intelligence, anchored by SABIC’s 4.01 million tons of capacity. The integrated Gulf system, advantaged by ethane priced at USD 1 to 2 per million BTU versus USD 4 to 6 globally, defined the cost curve for Asian and European converters. That cost advantage is now stranded behind a closed strait and force majeure declarations.

The Three Structural Shifts Already Visible

The first structural shift is the acceleration of U.S. ethane exports to Asia, alongside rising LPG flows into the region. China’s U.S. ethane imports reached 3.462 million tons in the first months of 2026, more than half of the full-year 2025 volume, with the United States now the sole supplier. The U.S. Energy Information Administration’s October Short-Term Energy Outlook forecast 14 percent ethane export growth in 2025 and 16 percent in 2026 before the conflict; actual 2026 growth will substantially exceed that. Chinese ethylene producers now view U.S. ethane as the preferred alternative due to its supply stability and cost advantage, according to Shi Linlin’s analysis reported by IDNFinancials. This is not a temporary substitution. The cracker reconfigurations and long-term offtake contracts being signed in Q2 2026 will lock in U.S. ethane dependency through 2035.

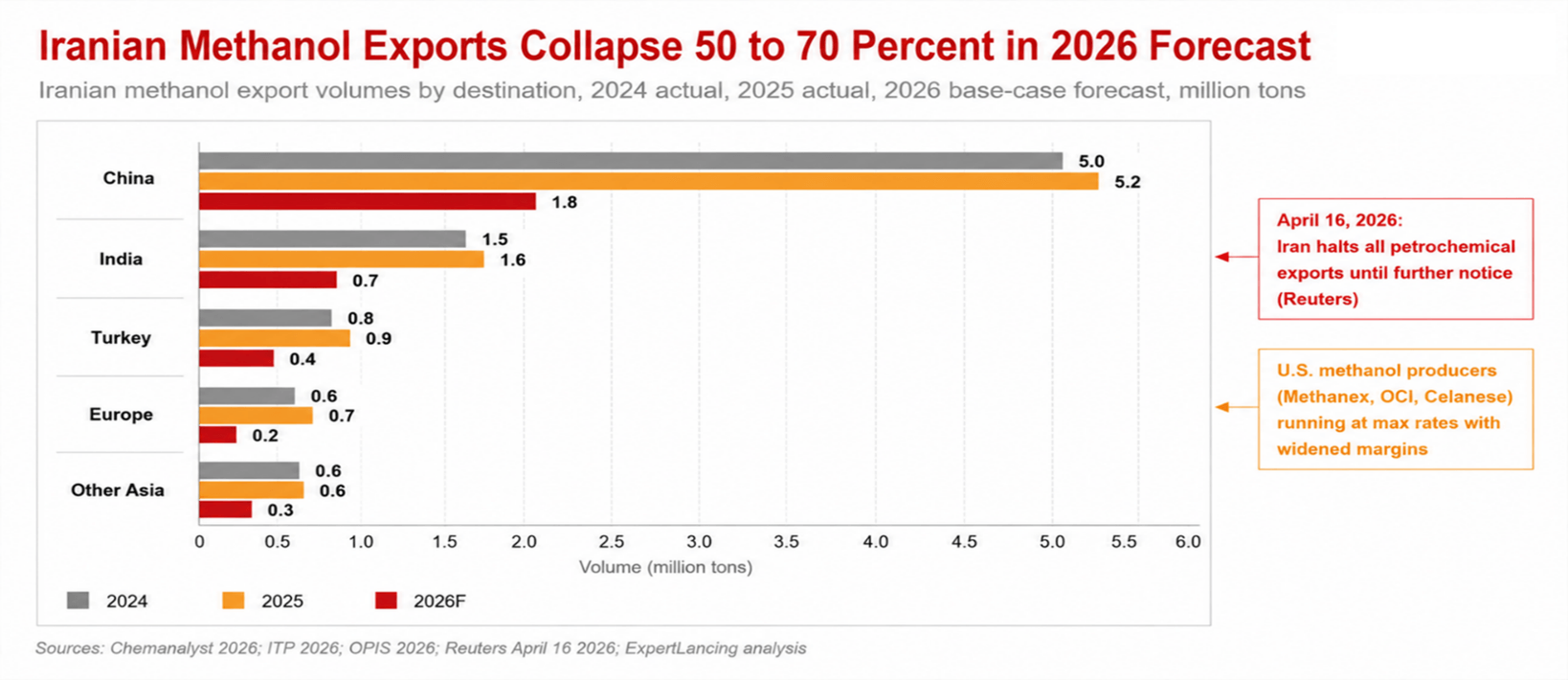

The second shift is the collapse of Iranian export optionality. Iran formally halted petrochemical exports on April 16, 2026, citing domestic stabilization and infrastructure damage. Discovery Alert estimates the halt disrupted approximately USD 13 billion in annual global supply. The U.S. Treasury announced new sanctions on April 24 targeting Chinese teapot refineries and Iran’s shadow fleet. Even if the conflict de-escalates, the combination of physical infrastructure damage, sanctions tightening, and counterparty caution suggests Iranian methanol, MEG, and polyethylene exports will return at 40 to 60 percent of pre-conflict levels through 2027, not 90 to 100 percent.

The third shift is European demand destruction, accelerating European petrochemical capacity rationalization that was already underway pre-conflict. Singapore naphtha at USD 1,000 per ton makes integrated European steam crackers structurally unprofitable. We estimate 1.5 to 2.5 million tons of European ethylene capacity faces permanent closure decisions in 2026, accelerating a rationalization already underway pre-conflict. The Fitch Ratings analysis published March 25, 2026 concludes the conflict will constrain chemical production and trade across naphtha, LPG, sulphur, and ammonia feedstocks. European converters that survive will increasingly source finished polymers from U.S. and Asian producers rather than crack their own.

The Methanol Squeeze Is the Sharpest Single-Product Story

Methanol deserves separate analysis because it concentrates the disruption. The methanol supply disruption is the sharpest single-product impact of the 2026 Iran conflict. Iran is the world’s second-largest methanol producer behind China, exporting 80 to 90 percent of its 9 to 10 million ton annual output. China alone imported 5 million tons from Iran in 2024. The March 2026 collapse in Chinese imports from the Middle East, documented by ITP, removed approximately 700,000 to 900,000 tons of monthly supply from the global balance. OPIS analysis confirms the impact extends beyond Iran to the broader Middle Eastern petrochemical supply chain.

Methanol downstream chains, including formaldehyde, acetic acid, MTBE, and methanol-to-olefins (MTO) units, are the immediate casualty. Chinese MTO operating rates fell sharply in April 2026, transmitting cost pressure into polyolefins. U.S. methanol producers (Methanex, OCI, Celanese) are running at maximum rates with widened margins. The 2026 to 2028 window will likely see at least two new methanol export project FIDs in the U.S. Gulf and one to two in Trinidad, locking in non-Iranian supply for the next decade.

Implications for Decision Makers

For Asian producers, particularly in China, India, South Korea, and Japan, the immediate priority is feedstock diversification. Lock in U.S. ethane and LPG offtake contracts now, before pricing power consolidates around the three to four U.S. export terminal operators. Specifically, Chinese producers including Wanhua, Satellite Chemical, and Sinopec should accelerate ethane cracker conversion programs and secure dedicated VLEC (very large ethane carrier) capacity.

For Gulf producers (SABIC, Aramco, ADNOC, QatarEnergy), the conflict has paradoxically strengthened long-term pricing power but exposed logistics fragility. Strategic priority is dual-coast export capability, accelerating Red Sea and Indian Ocean export infrastructure to reduce Hormuz dependency. The 24 to 36 month investment cycle in alternative export terminals will define competitive positioning through 2035.

For European players (BASF, INEOS, LyondellBasell European assets, Borealis), the rationalization decision can no longer be deferred. We estimate 1.5 to 2.5 million tons of European ethylene capacity will be announced for permanent closure in 2026 to 2027. The strategic question is not whether to close, but which assets to convert to specialty and circular feedstocks versus shutter entirely.

For U.S. producers (Dow, LyondellBasell, Westlake, ExxonMobil Chemical, Chevron Phillips), the window to expand ethane export capacity and lock in 10 to 15 year Asian offtake is open now. Expect two to four new ethane export terminal FIDs in 2026 and 2027 along the U.S. Gulf Coast.

For downstream converters and CPG buyers, contract negotiation strategy must shift from spot exposure to indexed long-term agreements covering 60 to 70 percent of demand. Single-source dependencies on any Middle Eastern supplier should be capped at 20 percent of any single feedstock or polymer line.

For investors, U.S. midstream and ethane export infrastructure (Enterprise Products Partners, Energy Transfer, Targa) offers the cleanest exposure to the structural reset. Gulf integrated names will outperform on near-term pricing but face logistics overhang. European chemicals will continue to derate.

What to Watch in the Next 12 to 24 Months

First, the Strait of Hormuz reopening timeline. The Pentagon’s April 21 estimate of six months to fully clear the strait points to a Q4 2026 normalization in the base case. A delayed reopening into 2027 or a re-escalation would push another 4 to 6 million tons of ethylene capacity into force majeure or permanent closure decisions.

Second, U.S. ethane export terminal FIDs. Watch for announcements from Enterprise Products, Energy Transfer, and Targa on second-wave terminals at Morgan’s Point, Nederland, and new sites. Two or more FIDs by Q1 2027 would signal a permanent structural shift; zero FIDs would indicate the market expects faster Iran normalization.

Third, the Iranian petrochemical export resumption rate. The April 16 export halt and Treasury sanctions create a multi-variable equation. Our base case is 40 to 60 percent of pre-conflict export volumes by end-2027. A return above 75 percent would compress global methanol and MEG margins; a return below 30 percent would lock in the structural reset.

Conclusion

The 2026 Iran conflict is not a transient price event. It is a structural reset of the global petrochemical feedstock map, and a lasting petrochemical feedstock disruption in the global feedstock supply chain, removing 22 million tons of potential ethylene output, severing roughly USD 13 billion in annual Iranian export flows, redirecting Chinese feedstock dependency to the U.S., and accelerating European capacity rationalization that was already overdue. It is also reshaping Iran petrochemical exports, methanol flows, and ethylene supply disruption risk across Asia and Europe. The winners of the 2026 to 2030 cycle will be defined less by who has the lowest cost feedstock and more by who controls the logistics corridors that move global petrochemical feedstock supply to converters. Decision makers should plan for a feedstock map in 2030 that looks materially different from the one that existed on March 1, 2026.

For petrochemical market intelligence, feedstock risk mapping, or supply chain strategy support, connect with ExpertLancing.