A historic geographic rebalancing is reshaping the world’s automotive industry. While the established markets of North America and Europe wrestle with saturation, mounting regulatory demands, and evolving buyer tastes, India has emerged as the sector’s primary growth engine. The country crossed a notable threshold in 2026, surpassing Japan to become the third-largest car market anywhere, with sales climbing 15.6% year-to-date and accounting for a 6.6% share of vehicle sales worldwide. Far from a passing statistic, the achievement marks a genuine restructuring of the global automotive hierarchy.

What matters most to industry players now is not whether India’s rise continues, but the pace at which it reaches second place worldwide, along with the implications for investors, manufacturers, suppliers, and technology providers. Forecasts put passenger vehicle sales at 6.1 million units by 2030, while the broader market could approach 10 million units as the country pushes toward the runner-up position globally. With those numbers in view, identifying the likely winners and the forces shaping this shift has become central to any serious strategic planning.

The Growth Trajectory: From Aspiration to Achievement

Over the last ten years, India’s automotive market has transformed considerably. The passenger vehicle segment, which logged roughly 4.1 million units in 2023, is on track to hit 6.1 million units by 2030, a pace equal to a compound annual growth rate of 5.6%. Factor in commercial vehicles, two-wheelers, and three-wheelers, and the market as a whole is set to grow from 5.1 million units in 2023 to 7.5 million units by 2030, with certain forecasts indicating it could near 10 million units should conditions prove favorable.

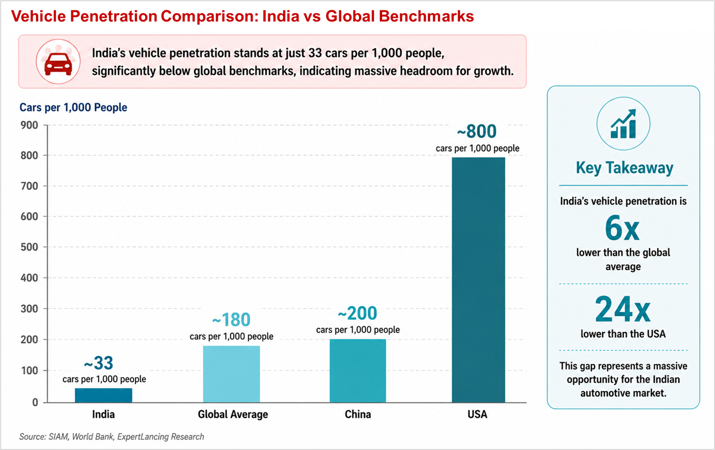

Behind this trajectory sits one of the strongest demand foundations found anywhere in the world. India counts just ~33 cars per 1,000 people at present, against more than 800 in the United States and somewhere near 200 in China. With per capita incomes on the rise and the middle class widening, that ownership gap amounts to a growth runway stretching across decades, something few other large economies can offer.

Policy Architecture: Building an Enabling Ecosystem

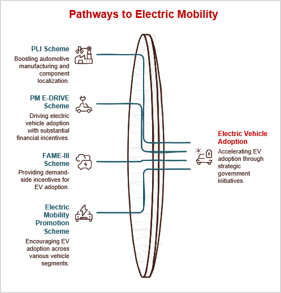

India’s government has placed the automotive sector at the center of its strategy, building a strong policy framework that is speeding up both market growth and the shift toward new technologies. The Production Linked Incentive (PLI) Scheme for Automobile and Auto Components, cleared in September 2021 with a budget of ₹25,938 crore, was later doubled to ₹5,940 crore in February 2026 and carried forward through March 2028. Its purpose is to lift manufacturing of Advanced Automotive Technology products and to drive deep localization of critical components.

The PM E-DRIVE scheme, introduced in October 2024 with a budget of ₹10,900 crore, serves as India’s overarching push to quicken electric vehicle uptake. Working alongside it, the FAME-III scheme and the Electric Mobility Promotion Scheme 2024 offer demand-side incentives that are lifting EV adoption across two-wheelers, three-wheelers, and four-wheelers. Together, these measures are expected to deliver the government’s goal of a 30% electric vehicle share of total vehicle sales by 2030.

The EV Transition: India’s Fastest-Growing Segment

Of all the dimensions of India’s automotive shift, the electric vehicle segment is proving the most dynamic. The country reached a notable mark with 100,000 EVs sold in calendar year 2024, rising from 82,688 units the year before. Electric three-wheelers hit a record 741,420 units in FY25, even as the electric passenger vehicle market climbs at an exponential pace.

Across the first 11 months of FY26, Tata Motors moved 69,765 electric passenger vehicles, a 32% year-on-year increase that translated into roughly 38-40% of the market. Rounding out the field are JSW MG and Mahindra & Mahindra, and together these three account for close to 86% of electric passenger vehicle sales. Maruti Suzuki’s arrival in the EV space with the e-Vitara points to electric mobility entering the mainstream.

Investment Flows and Manufacturing Localization

How much capital is moving into India’s automotive sector says a great deal about the confidence investors worldwide place in its growth prospects. Between April 2000 and March 2025, the industry drew USD 37.85 billion in FDI inflows, placing it among the top recipients of any sector. Among the more recent pledges is Nissan’s commitment of ₹6,496 crore over the coming two years, earmarked for several new model launches and added manufacturing capacity.

Within the PLI-Auto Scheme, total investment had reached ₹35,657 crore as of 30 September 2025, creating 48,974 jobs and generating incremental sales of ₹32,879 crore. The scheme zeroes in on Zero Emission Vehicles, Battery Electric Vehicles and Hydrogen Fuel Cell Vehicles among them, with incentives running through FY 2026-27.

Supply Chain Transformation: The Auto Components Opportunity

India’s emergence as a global automotive hub is driving a parallel transformation in the auto components sector. According to NITI Aayog projections, auto component production could reach USD 145 billion by 2030, with electric vehicles driving 40% of growth. Automobile exports from India rose 19% in FY25 to over 5.3 million units, led by robust demand for passenger vehicles, two-wheelers, and commercial vehicles in global markets.

This supply chain expansion is creating opportunities across the entire value chain, from raw materials and precision components to advanced electronics and software. The government’s Automotive Mission Plan 2016-26 has established a development roadmap that targets positioning India as a global hub for automotive manufacturing and research and development.

Strategic Implications: Who Wins in the New Market Order?

Moving from 4 million to 10 million vehicles a year will produce clear winners in several corners of the automotive ecosystem. Homegrown manufacturers that combine strong SUV lineups with electric vehicle expertise, Tata Motors, Mahindra & Mahindra, and Maruti Suzuki chief among them, stand to absorb the bulk of the volume gains. Global OEMs that have localized their production and built product strategies tailored to India, such as Hyundai Motor India and Kia, are equally well placed to gain as the market widens.

The picture is much the same on the supply side, where component makers skilled in advanced materials, precision engineering, and electronics are seeing demand intensify. The auto components industry turned over close to ₹6.73 lakh crore in FY2025, and that growth is gathering speed as the localization requirements built into the PLI scheme begin to bite.

Future Outlook: Navigating the Path to 2030

The trajectory toward 10 million vehicles annually is not without challenges. The industry must navigate supply chain disruptions, regulatory transitions including the upcoming CAFÉ 3 norms effective April 2027, and the infrastructure requirements of mass electric vehicle adoption. However, the structural drivers like rising incomes, low vehicle penetration, favorable demographics, and supportive policy frameworks, remain intact.

By 2030, projections suggest India will not only be the world’s second-largest auto market but also a major export hub. The electric vehicle industry is likely to touch ₹20,00,000 crore (USD 234 billion) and create approximately five crore jobs. With vehicle penetration expected to reach 72 vehicles per 1,000 people by 2025 and continue climbing thereafter, the growth runway extends well beyond the current decade.

Conclusion: A Defining Decade for Indian Automotive

India’s ascent from 4 million to 10 million vehicles a year amounts to far more than a bigger market. It marks the rise of a new global automotive order. For manufacturers, suppliers, investors, and technology providers alike, the winners will be those who see that India’s market is not simply expanding but changing in character, as electrification, localization, and digitalization rewrite the rules of competitive advantage.

As India positions itself to become the world’s second-largest auto market, the opportunity extends beyond volume growth to value creation across the entire mobility ecosystem. The next decade will determine which stakeholders successfully capture this once-in-a-generation transformation.