Cloud infrastructure isn’t just growing right now, it’s being remade from the inside out. The market touched roughly $917.9 billion in 2026 and looks set to cross the trillion-dollar mark before the year closes, but the bigger story is how much its makeup has changed in just two years, more than in the decade before that. What’s pushing this growth now has little in common with the workload-migration boom that defined cloud’s earlier years. AI inference running at production scale, governments demanding data sovereignty, power-grid limitations, and chipmakers building AI-specific silicon into their own stacks, these are structural shifts, not passing trends. Providers and enterprises that keep treating them as side issues, rather than questions that need a real strategic answer, are setting themselves up for a disadvantage that won’t be easy or cheap to undo later.

Below are identified ten imperatives that collectively define this reconfiguration. Ranked by impact score and evaluated across multiple provider tiers, they offer a disciplined lens for understanding where competitive advantage is being built and where it is being quietly eroded.

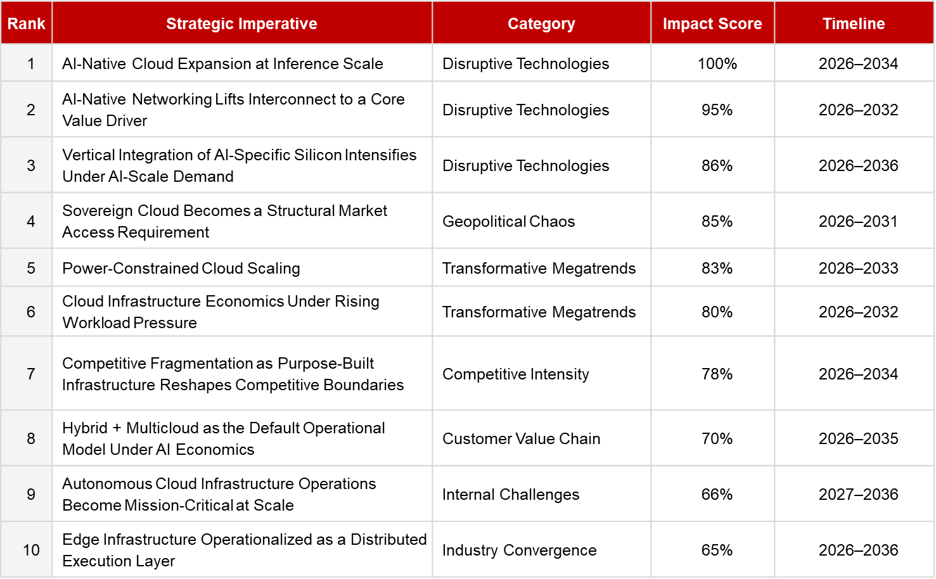

The Top 10 Strategic Imperatives at a Glance

When Infrastructure Becomes Strategy: The AI-Native Transition

The three highest-ranked imperatives share a common thread they are all consequences of enterprises moving generative AI from controlled experimentation into full-scale, revenue-generating production. As this transition accelerates, the infrastructure demands it generates are qualitatively different from anything cloud providers have previously optimised for.

AI-related cloud spending now accounts for 19% of total cloud expenditure in 2026, up from just 8% in 2023, and for the first time, inference workloads have surpassed model training in total compute consumption. This matters because inference is continuous, latency-sensitive, and economically demanding in ways that sporadic training runs are not. Cost per token, latency consistency, and sustainable unit economics have become board-level concerns, not just technical parameters.

Networking is feeling this pressure acutely. Distributed AI training and high-concurrency inference are generating unprecedented east-west traffic volumes across GPU clusters, making cloud networking a direct determinant of AI cost and performance rather than a supporting layer. Providers that operate on legacy, capacity-constrained fabrics face inference bottlenecks that translate directly into competitive disadvantage.

Control over AI-specific silicon completes this trio. The Big Four hyperscalers, Amazon, Google, Microsoft, and Meta – collectively plan nearly $700 billion in capital expenditure in 2026, with the majority directed at AI infrastructure including proprietary accelerators. Smaller cloud operators without silicon ownership face mounting margin pressure and supply uncertainty as this arms race intensifies. For regional and AI-native providers, the strategic response is not silicon ownership but rather deployment optimisation, workload specialisation, and long-term supply agreements that reduce external dependency.

Sovereignty Is No Longer Optional

What began as a regulatory compliance burden in Europe has evolved into a global structural requirement for cloud market access. Governments in the European Union, India, the Middle East, and Southeast Asia are mandating that cloud workloads handling sensitive data in public sector, financial services, healthcare, and critical infrastructure operate under locally controlled, jurisdictionally ring-fenced architectures. Providers that cannot demonstrate clear data residency enforcement and legally separated operational models are simply ineligible for these contracts.

The commercial scale of this shift is significant. The global sovereign cloud market was valued at over $117 billion in 2025 and is projected to grow at a compound annual rate of over 24% through 2033. In October 2025, the European Commission published its Cloud Sovereignty Framework, defining binding sovereignty objectives for institutions procuring cloud services, a development that directly shapes how hyperscalers and regional operators must structure their European infrastructure. The strategic implication is clear: sovereign readiness is now a revenue prerequisite, not an optional product feature.

Power and Cost Discipline as the New Competitive Variables

Energy has emerged as the binding constraint on cloud infrastructure expansion in a way that capital availability alone cannot resolve. The International Energy Agency reports that data centre electricity demand surged 17% in 2025, with AI-focused deployments growing even fasterm. It is estimated that power shortages will restrict expansion at 40% of AI data centres by 2027. Site selection has been transformed from a function of latency and fibre access into a search for available megawatts, a structural shift that is reshaping where infrastructure gets built and which regions can attract capital investment.

The economics imperative sits directly alongside this energy challenge. AI workloads generate burst-driven GPU demand and persistent inference-serving requirements that dramatically increase infrastructure cost variability. The proportion of organisations treating AI as an active FinOps concern jumped from 31% in 2024 to 63% in 2025, the sharpest two-year increase the FinOps Foundation has recorded, signalling that cloud cost governance has moved decisively from IT operations into executive decision-making. Providers capable of delivering transparent, predictable AI-scale cost structures, not just raw compute access – will retain enterprise relationships as procurement discipline continues to harden.

Fragmentation, Flexibility, and Autonomous Operations

The assumption that cloud infrastructure competition would consolidate around a handful of dominant hyperscalers is being actively challenged. Purpose-built AI providers are entering high-value workload domains, regulated healthcare data processing, financial AI inference, autonomous systems by offering tightly integrated compute, silicon, networking, and AI software frameworks that general-purpose hyperscale platforms were not originally designed to deliver. This is competitive fragmentation in the truest sense: demand is being redistributed across provider tiers based on workload fit rather than incumbent scale.

Enterprises are responding with deliberate multi-vendor strategies. Eighty-seven percent of organisations now run a multi-cloud strategy, and 73% operate hybrid cloud estates, but the motivations have deepened beyond risk mitigation. AI scale, sovereignty requirements, and pricing dynamics make single-provider dependency both economically and operationally restrictive. Managing this distributed complexity, however, demands automation that manual operations teams cannot provide. Cloud providers are responding by embedding AI-driven orchestration, enabling real-time workload balancing, self-healing capabilities, predictive capacity planning, and automated cost controls directly into core infrastructure layers. Providers that rely on reactive, human-intensive operations risk margin leakage that compounds with every new workload at scale.

Edge Infrastructure Steps into the Execution Tier

The edge computing imperative scores lowest among the ten, but its directional significance should not be underestimated. As AI inference moves into latency-sensitive operational environments industrial automation, connected healthcare, autonomous logistics, real-time retail analytics, centralised data centres face a physics constraint that cannot be engineered away. Applications requiring sub-50-millisecond response times cannot be served from a distant cloud region, full stop.

The global edge computing market is reflecting the pace at which distributed infrastructure is moving from a niche capability into a standard architectural tier. Cloud providers that integrate edge through seamless core-to-edge orchestration, telecom partnerships, and regionally distributed compute zones are positioning for workload segments that traditional hyperscale architectures will increasingly struggle to serve on cost and latency grounds.

The Growth Trajectory and What It Demands

The aggregate investment picture validates the structural weight of these imperatives. The global cloud infrastructure market is driven by AI workloads, hybrid adoption, and sovereign infrastructure expansion. But this growth will not be evenly distributed. Providers that adapt architecturally building AI-native capacity, sovereign compliance blueprints, energy-efficient infrastructure, and autonomous operational capabilities will capture disproportionate share. Those that remain structured primarily around general-purpose compute and traditional enterprise workloads will face margin compression and declining relevance in the segments that generate incremental growth.

Conclusion

The ten strategic imperatives identified for 2026 are not isolated trends, they are interconnected forces reshaping the economics, architecture, and competitive structure of cloud infrastructure simultaneously. AI economics have displaced general-purpose compute as the primary determinant of cloud competitiveness. Energy and sovereignty have moved from the periphery of infrastructure planning to its strategic core. Competitive fragmentation and operational complexity are demanding architectural reinvention across all provider tiers, from global hyperscalers to AI-native specialists.

For business leaders, the central question is no longer whether these shifts are happening, they are demonstrably underway. The more pressing question is whether the organisation is adapting at the speed and depth this market now demands. Those that align capital allocation, technology roadmaps, and operational models to these ten imperatives will be positioned to lead the next phase of AI-driven infrastructure expansion. Those that do not will find the gap increasingly difficult to close.