GLP-1 is driving a structural shift in food consumption behavior, reshaping household food demand. The winners will compete on satiety per dollar rather than indulgence per occasion.

The end of consumption-led growth

For decades, the food industry was driven by a core growth model: encourage higher consumption, more often. Oversized portions, frequent snacking, and hyperpalatable products turned volume expansion into the industry’s primary business model.

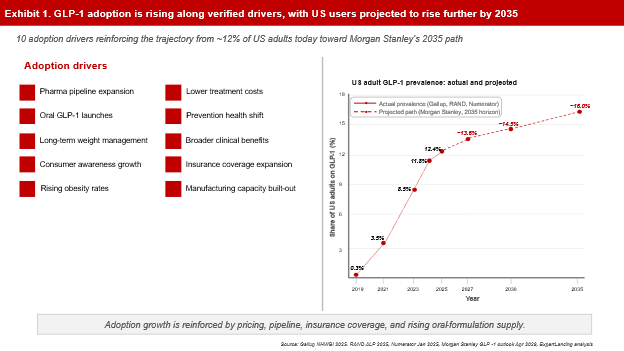

That model is now being challenged by GLP-1 drugs such as Ozempic, Wegovy, and Mounjaro. Originally developed for diabetes management, these therapies have gained mass adoption for weight management, suppressing appetite and reshaping food purchasing and consumption patterns broadly. GLP-1 adoption is projected to continue expanding through 2035, driven by improving drug accessibility, rising obesity prevalence, broader clinical applications, and growing consumer awareness, with Morgan Stanley forecasting sustained long-term market growth. The signal is a major long-term shift in healthcare and food consumption patterns (Exhibit 1).

GLP-1-driven calorie reduction trends could lower overall food consumption volumes by more than 10 percent, while Circana forecasts that GLP-1 users could account for 35 percent of US food and beverage units sold by 2030, up from 23 percent today.

The shift is no longer a limited health trend. It is a structural consumption reset. The industry is moving from indulgence-led consumption toward more intentional, consciousness-led eating behavior.

Appetite suppression is reshaping consumer behavior

High adoption of GLP-1 therapies has produced not just lower calorie intake but a structural behavioral change in how consumers approach food. As “food noise” declines, users report reduced attention to cravings, snacking, and emotional eating, weakening the established eating habits that historically fueled large parts of the packaged food and restaurant economy.

This shift is already reshaping purchasing behavior. Consumers are moving away from craving-driven purchases toward protein-rich, nutrient-dense, and functional foods, while cutting back on frequent snacking occasions. The impact extends beyond grocery retail into restaurants and hospitality, signaling that demand softness is spreading across the broader food ecosystem.

For brands, this represents a structural realignment challenge rather than a short-term consumption slowdown. As GLP-1 therapies continue altering appetite patterns, portion sizes, and consumption frequency, competition will increasingly depend on maintaining relevance within fewer, more intentional consumption occasions rather than maximizing consumption levels or shelf visibility.

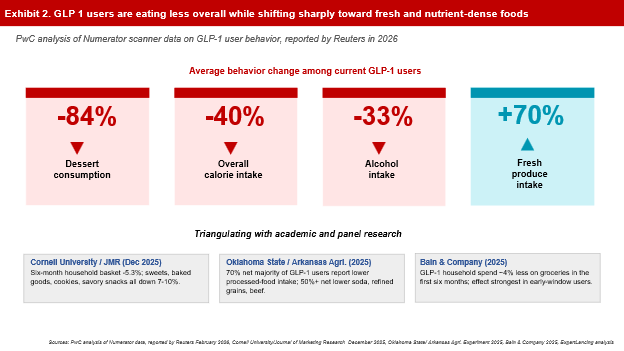

GLP-1 adoption is fundamentally reshaping consumer eating behavior. Users are becoming more intentional about food choices, reducing impulse-driven consumption such as desserts and alcohol while prioritizing fresher, nutrient-dense options. The shift signals a move away from habitual, volume-led eating toward more conscious, utility-driven consumption (Exhibit 2).

The emerging “satiety economy”

The next phase of GLP-1 disruption is not simply lower food consumption. It is the growth of a “satiety economy,” a market where value is anchored to nutritional efficiency rather than purchase volume. As reduced appetite reshapes consumption habits, consumers are becoming more selective about what is worth eating, prioritizing products that deliver protein, functional value, and sustained satiety.

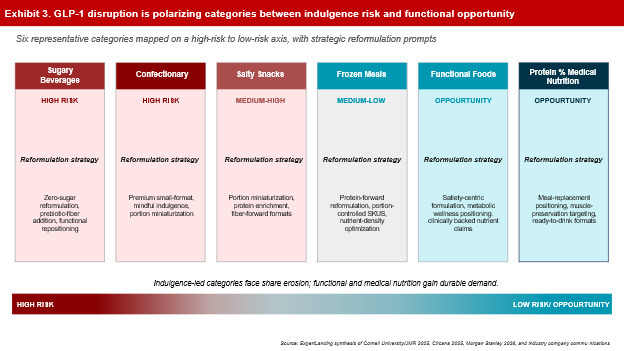

This creates a clear market split. Indulgence-led food segments such as confectionery, salty snacks, and sugary beverages face accelerating pressure as craving-driven purchases fall. Meanwhile, functional nutrition, protein-rich foods, and medical nutrition categories gain sustained market strength (Exhibit 3).

The growth opportunity is not in selling larger quantities of food. It is in selling value-added food. Consumers are prioritizing ingredient quality, nutritional value, and satiety per meal, which can make premium smaller portions more profitable than conventional high-volume formats.

Redesigning food for reduced appetite capacity

GLP-1 adoption is shifting food innovation toward nutrient-dense, smaller-format products. As appetite capacity declines and protein prioritization rises, brands must focus on delivering maximum nutritional efficacy within minimal serving sizes.

In response to accelerating GLP-1 demand, the leading food companies are developing satiety-centric product reformulations built on three strategic pillars:

- Protein, fiber, and nutrient enrichment: GLP-1-influenced consumption is boosting demand for ingredients such as whey, rice, and pea proteins, alongside functional fibers like resistant dextrin and chicory inulin, to support muscle retention, hunger management, digestive health, blood glucose regulation, and nutrient-dense smaller-format nutrition.

- Micronutrient (vitamin and mineral) fortification: Lower calorie intake is raising the importance of vitamin and mineral density, pushing brands toward science-backed fortification approaches that maximize nutritional value per serving.

- Sensory optimization: As nausea sensitivity and taste intolerance become more common among users, product innovation is shifting toward smoother textures, easier digestion, and milder flavor systems rather than conventional hyperpalatable profiles.

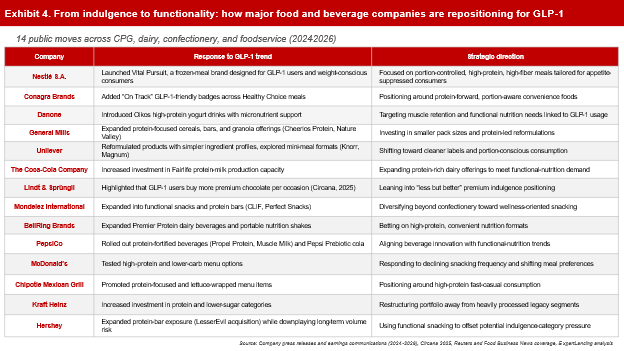

Major food and beverage companies are rapidly repositioning their portfolios around the GLP-1-driven shift toward protein-rich, portion-controlled, and functional nutrition. The industry response is increasingly centered on nutrient density, smaller-format consumption, cleaner-label reformulation, and wellness-oriented product innovation, signaling a broader transition from indulgence-led growth to satiety-focused consumption models (Exhibit 4).

GLP-1 is reshaping packaging, retail, and foodservice

The GLP-1 trend is forcing food manufacturers to rethink not only product design but the entire consumption ecosystem. In the emerging satiety economy, larger packs and quantity-driven offerings are giving way to exact-portion, nutrient-dense, single-serve formats tailored for smaller appetites and intentional eating occasions. Packaging is increasingly being repositioned from a branding surface into a nutritional communication platform, with brands emphasizing protein, fiber, satiety, and functional value rather than quantity.

This transition is already visible across retail and foodservice. Retailers including Ocado, Morrisons, Asda, Co-op, and Iceland have introduced GLP-1-friendly assortments and nutritionally balanced smaller meals, while foodservice operators such as McDonald’s, Subway, and Panera Bread are testing high-protein, reduced-portion menu formats. Cornell University and Circana data indicate that limited-service restaurant spending among consistent GLP-1 users has declined by roughly six to eight percent, highlighting the growing pressure on traditional high-frequency consumption models.

At the same time, labeling and merchandising are emerging as new competitive battlegrounds. While brands remain cautious around explicit GLP-1 health claims, the market is rapidly shifting toward satiety-aligned positioning built on high-protein, nutrient-dense, and portion-smart messaging.

Future outlook: personalization, companion nutrition, and the next frontier

The first phase of GLP-1 food adaptation has been reactive: labeling, limited reformulation, and portion resizing. The second phase, now emerging in 2026, is proactive and strategically differentiated. Three vectors will define it.

- Build GLP-1 companion nutrition as a distinct category. Nestlé Health Science’s framework of lean-muscle preservation, digestive upset management, and micronutrient replenishment provides a template for medically complementary nutrition platforms. These are not generic “healthy food” claims; they are products designed to address the physiological consequences of GLP-1 pharmacology. Companies that invest in the clinical substantiation behind these platforms will build durable competitive moats.

- Design personalized nutrition architectures around the GLP-1 user journey. Industry experts including Danone’s health-and-science leadership note that the GLP-1 consumer is not a monolith. Nutritional needs in week two of injection therapy differ materially from those of a long-term maintenance user. Brands that build product systems spanning this journey, from initial appetite adjustment through long-term weight management to potential drug discontinuation, will build loyalty that transcends any single SKU.

- Develop natural GLP-1 stimulation through food reformulation. Peer-reviewed research confirms that soluble fiber and specific proteins can stimulate endogenous GLP-1 secretion from intestinal L-cells. This creates a secondary market opportunity: foods designed not just for GLP-1 drug users, but for the wellness mainstream seeking to enhance their own appetite hormone response. Expected outcome: market expansion beyond the medicated minority.

The companies that will define the GLP-1 era in food are not those making the quickest label changes. They are those undertaking the harder work of structural reformulation, clinical partnership, and consumer journey design. The appetite is not disappearing. It is being redesigned. The food industry must redesign with it.

Key takeaways

- GLP-1 adoption has reached 12.4 percent of US adults in late 2025, reshaping markets and signaling a structural shift in long-term consumer behavior.

- Consumer preferences are shifting toward nutrition-dense meals. Product innovation is moving toward foods that support digestive health and deliver high protein, fiber, and micronutrients per serving.

- Leading food and beverage players, including Nestlé, Conagra, Danone, and PepsiCo, are reformulating and repositioning their portfolios to align with the new nutrition-focused demand.

- Newly initiated GLP-1 users spent about 22 percent more in dollars during their first 1-3 months on therapy, while household grocery baskets contract by 4 to 6 percent over the first six months. This combination creates dual pressure on food companies to defend volume while trading up on value.