Key Takeaways

- The global smart grid market is expected to reach $238.63 billion by 2035 with 17% CAGR and a sharply rising share of emerging economies’ deployment.

- India has rolled out 47.6 million smart meters and has crossed the 52% non-fossil energy capacity mark as of early 2026, making it the world’s second-largest renewable energy growth market.

- State Grid of China has allocated RMB 4 trillion ($548B) of grid investments between 2026 and 2030, a 40% boost from its previous five-year plan and a new global record.

- Up to 40% of the total potential solar energy in the world is located in Africa by 2050; 23% of all the households in 34 African nations are using electricity from non-grid sources.

- The Latin American smart meter market will experience 21.7% CAGR on its way to 38.4 million units in 2028; one year ago, Brazil doubled its solar energy generation capacity.

- The US will see 2,600 GW and Europe – 1,700 GW of clean energy projects stuck in grid queues; the problem is not money but regulations.

Introduction

It seemed obvious for most of the last century that the logic of energy infrastructure was predetermined; while the richer countries would lay out the networks, the others would wait and eventually catch up. The US and Europe established the standards, paid for the power plants, and constructed the transmission lines. The developing countries hoped someday to be able to join the ranks of energy-rich countries. This scenario is outdated, and even reversed.

Nowadays, the countries that are advancing their technologies and implementing smart grids with the greatest speed are not limited to Washington or Brussels. While in the US, 2,600 gigawatts worth of clean energy projects remain stuck on connection queues, double that of all installed energy sources in the country, China, India, Africa, and Brazil are independently writing a new book of rules for the industry.

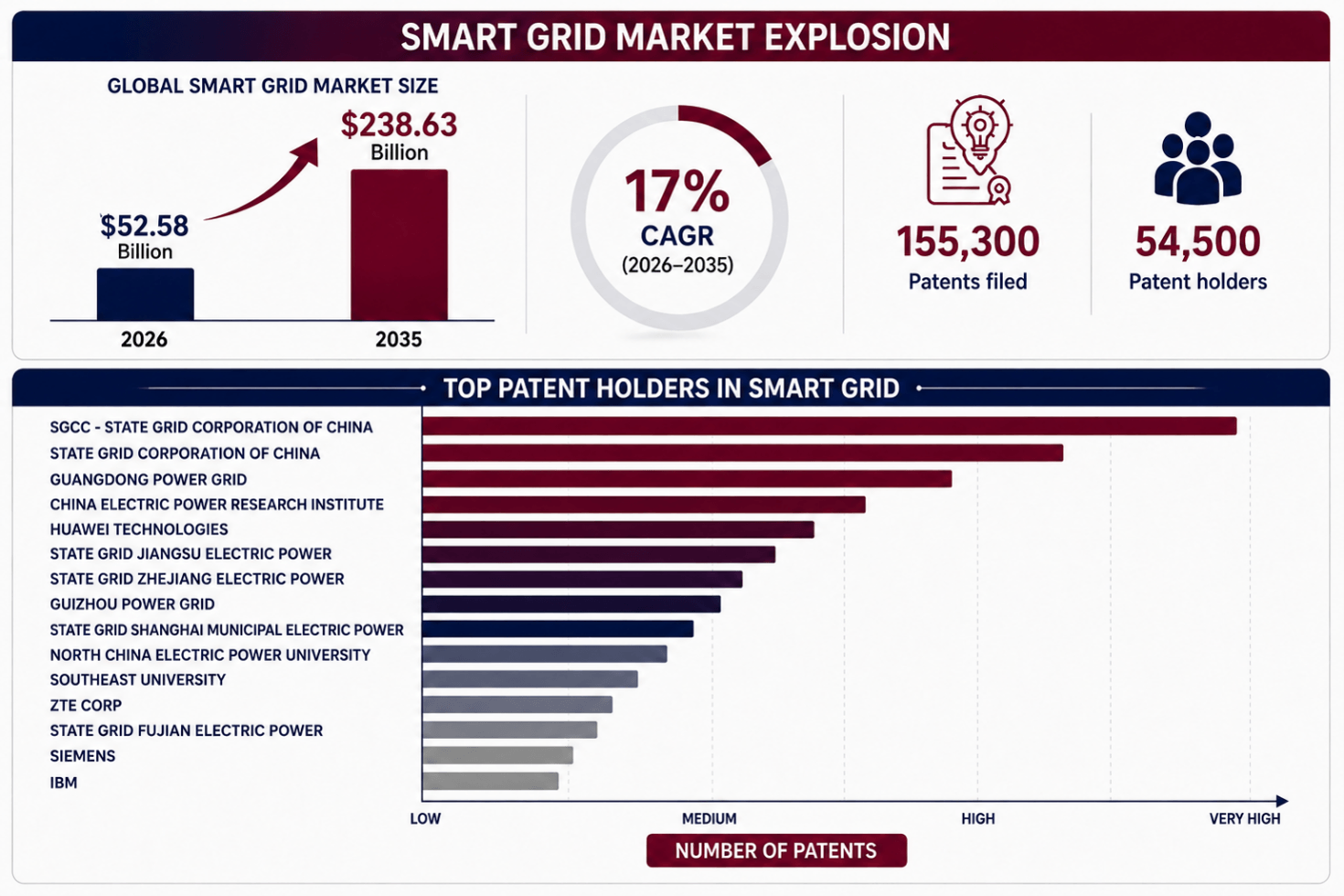

The worldwide smart grid market, estimated at around $52.58 billion in 2026, is projected to grow up to $238.63 billion by 2035, with a CAGR of 17%. The level of innovation in the industry is very high: 155,300 patents have been filed in the smart grid area by 54,500 patent holders, and the rate of patent filings per year is around 6.92%. Notably, China ranks first globally in smart grid patent filings, reflecting its strong focus and leadership in this sector. As the industry evolves, the challenge is no longer just building megawatts; it is managing variability at scale.

The West’s Grid Is Trapped by Its Own Success

In the paradoxical situation in which the Western world finds itself regarding energy, there lies an ironic twist. While it is precisely those countries that have developed and sustained the present electrical infrastructure, their dependence on it now limits them in ways never before seen.

As shown in the report entitled ‘Electricity 2026’ by the International Energy Agency (IEA), there are already 2,500 gigawatts of renewable energy projects waiting in line for grid connections worldwide: 2,600 gigawatts in the US and almost 1,700 gigawatts in 16 European countries. The primary bottlenecks are not technological limitations but regulatory and administrative challenges. Lengthy permitting processes and resistance related to land use have emerged as major barriers to expanding grid infrastructure in both regions.

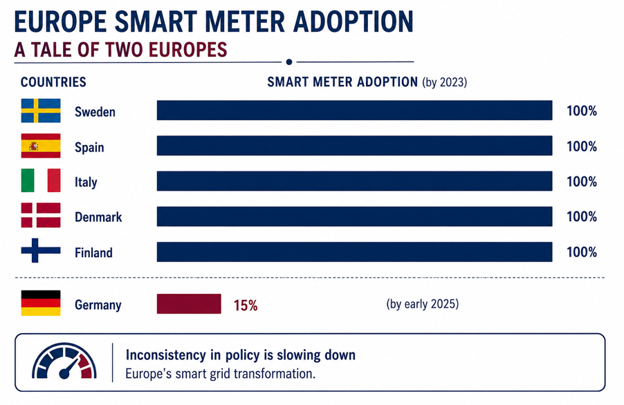

Inconsistency in Europe adds to the situation. Adoption statistics for smart grids in Europe, based on the IIIEE Energy Blog (April 2026), show that while countries like Sweden, Spain, Italy, Denmark, and Finland installed all of their smart meters by 2023, the German government implemented its national mandate in the same period but managed only 15% adoption until early 2025. Additionally, the worldwide expenditure on grids was estimated at over $470 billion in 2025, of which the US invested $115 billion. Nonetheless, despite the massive investments, there is no acceleration in deployments.

India: The World’s Most Ambitious Grid Transformation

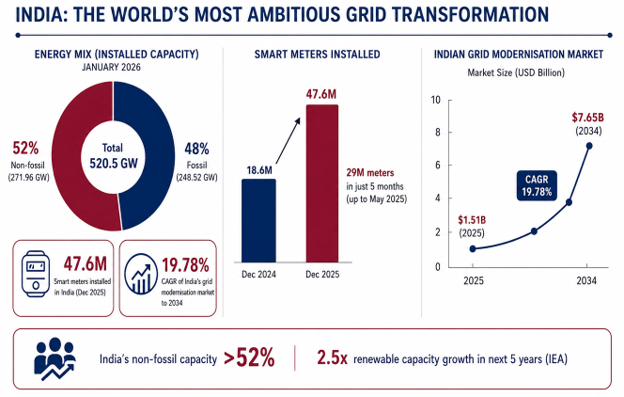

For the first time in history, in January 2026, non-fossil-based sources of energy, which include 263.2 GW of renewable power and 8.78 GW of nuclear power, account for over 52% of India’s total installed capacity of 520.5 GW. “Breaking through 50 percent fundamentally changes how the grid needs to work,” said Frost & Sullivan analysts in an April 2026 report. “The task isn’t simply to build megawatts anymore. It’s managing variability at scale.”

A total of 47.6 million smart meters have been installed in India as part of its National Smart Grid Mission by the end of 2025. 29 million meters were rolled out in just five months up to May 2025. The smart meters allow for prepaid energy management, energy accounting at the feeder level, real-time energy usage data, and remote fault detection using SCADA/DMS.

The Indian grid modernisation market had a market value of US$ 1.51 billion in 2025 and is expected to reach US$ 7.65 billion by 2034 at a CAGR of 19.78%, which is nearly thrice the global smart grid market CAGR.

The Renewables 2025 report by the International Energy Agency (IEA) indicates that India will be able to become the second-largest growth market for renewables globally with a total capacity to increase by 2.5 times in the next five years.

The Indian grid modernization market has a CAGR of 19.78%, which is nearly thrice the global market CAGR. Currently, 47.6 million smart meters have been deployed, and India gets more than 52% of its power from renewable sources.

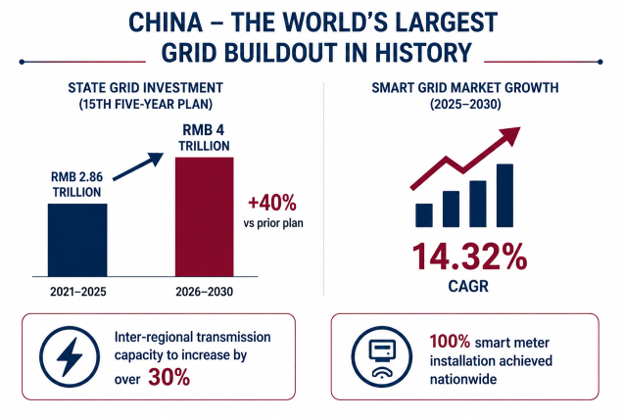

China – The World’s Largest Grid Buildout in History

China is implementing the largest grid development project in history. According to an announcement by the State Grid Corporation of China in January 2026, China’s fixed asset investments in the 15th Five-Year Plan period (2026-2030) would amount to RMB 4 trillion, which is a 40% rise compared to the preceding five-year period.

State Grid is to intensify its efforts to develop ultra-high voltage DC transmission corridors to transmit renewable energy generated from huge solar power plants and wind farms located in arid deserts and the Gobi region to coastal cities where there are many factories, thousands of kilometers away. The inter-regional transmission capacity will be increased by over 30% from the end of the previous plan period.

The growth rate for China’s smart grid network market is estimated to be at an impressive annual growth rate of 14.32%. This will enable the China Electricity Council’s target of total investment in smart grids to amount to CNY 4 trillion. China has also succeeded in making sure that it achieves 100% installation of smart meters all over the country; something that countries like Germany, having one of the biggest economies in Europe, have yet to achieve.

Africa and Latin America – Leapfrogging and Scaling

Africa and Latin America provide examples of two different but equally influential trajectories of grid innovation. The continent of Africa is skipping the grid paradigm entirely. In an article published in Science magazine (July 2025), scientists describe the requirements for a successful technological leapfrog. First, the technology must be proven and successful in developed countries. Second, the technology should have similar or even better performance than the existing technology. Third, it should make it possible to circumvent infrastructure. All these requirements are fulfilled by distributed solar energy and smart grids.

Kenya boasts the most solar panels per capita of all countries and has been the first African nation to utilize geothermal energy. By 2040, geothermal energy will constitute 50% of the total energy consumed in Kenya. Morocco has built one of the largest concentrating solar power stations in the world and aims at becoming an exporter of clean energy to Europe. According to Afrobarometer surveys conducted across 34 African nations, 23% of African households currently obtain electricity from non-grid sources, with 16% obtaining their electricity exclusively from non-grid sources. The continent has the capacity to generate 40% of global solar power and 10% of wind power by 2050.

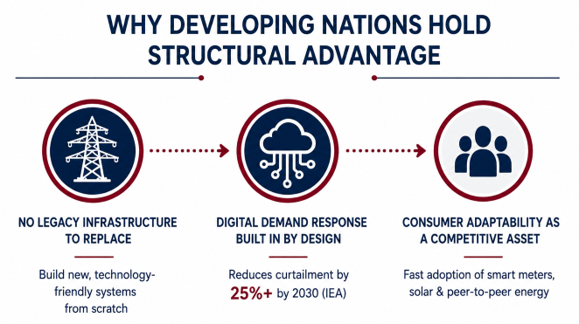

Why Developing Nations Hold the Structural Advantage

The efficiency of grid modernization in emerging countries has been attributed to three persistent structural strengths that traditional grids cannot afford despite adequate funding.

- No Legacy Infrastructure to Replace

In the US grid, there is some infrastructure from the 1950s and 1960s that needs upgrading. This would involve coordinating with utilities, compensating property owners, environmental impact assessments, and maintaining grid stability through the process. Developing countries have no such constraints and can establish an entirely new and technology-friendly system from the start.

- Digital Demand Response Built in by Design

According to IEA, demand response via digital means is capable of reducing curtailing of variable renewable energy sources by over 25% in 2030, resulting in increased system efficiency and cost savings for consumers. Countries building their smart grids for the first time will have an opportunity to incorporate features for demand response right from the start of construction.

- Consumer Adaptability as a Competitive Asset

The same adaptability that made M-PESA succeed has now become an even faster force for the adoption of prepaid smart meters, rooftop solar power, and peer-to-peer energy sharing in places where the existing players simply do not have the means or motivation to block innovation. As was highlighted in 2025 by researchers at Science, African consumers time and again surprised experts by successfully embracing new technology.

What the West Must Learn and Fast

World Resources Institute makes its position very clear – investment in global grids needs to grow annually from $410 billion in 2025 to around $600 billion in 2030 in order for the world to succeed on its climate and energy goals. However, the World Resources Institute equally notes that while the problem is not in financing, permitting delays and fragmented regulation are what prevent Western grid modernization.

The lessons emerging countries teach us are simple and replicable:

- Federal permit reforms. The biggest challenge for Western grid modernization is not technical but related to the permit process, which can be solved via federal permit reforms. Countries implementing national permitting reforms are able to build faster and cheaper.

- Modular solutions vs megaprojects. Developing countries are using modular building solutions that offer a great deal of flexibility when being upgraded, rather than one-point-of-failure mega-project approaches of the West.

- Combine efforts in expanding supply with an equal focus on demand flexibility. Grid balancing can be achieved equally well by managing load and applying demand response measures, as well as by adding generation resources, but with lower costs involved. India and Brazil are developing their grids, keeping these principles in mind.

- Mirror investment in data architecture to investment in the physical grid. Mandatory local content policy applied to data meters software by India demonstrates an advanced level of understanding that data intelligence is crucially important, just like the grid’s physical infrastructure.

- Learn lessons from the leapfroggers. Kenya, Morocco, and India are implementing smart grids at scale, not through pilots. The experience accumulated by them is one of the best sources of insights on smart grids development.

Conclusion

There is a new grid race leaderboard, and the West is not atop it. India has reached 52% non-fossil energy capacity. Africa is leapfrogging straight to decentralized grids. Brazil increased its solar power generation capacity tenfold last year alone.

The US has 2,600 gigawatts of clean energy stalled in development queues, while Europe is sitting on 1,700 gigawatts in 16 countries. Meanwhile, Germany has managed to equip 15% of households with smart meters in a decade of effort.

While access to capital, institutional capacity, and know-how were the main factors that helped the West be the grid race winner of the past century, these will not be enough in this one. Agility and flexibility, as well as the ability to experiment and move fast without being hindered by legacy infrastructure, are becoming ever more important. Annual investments in grids have to rise to at least $600 billion by 2030 to fight climate change, and doing so is going to require speed and humility in learning from other countries.

Closed-loop grid innovation is no longer something that countries of the developing world aspire to achieve, but an asset that they have learned how to export.

Recommendations for Stakeholders

Grid Permitting Reform and Regulatory Approvals Process: The national governments of both the US and the EU need to approach grid permitting reform on a par with military infrastructure. Preapproved corridors, federal-level centralized assessment, and standardized environmental impact assessments can reduce permit times from years to months – the most effective move possible.

Learn From China and India as Peer Examples Rather Than Rivals: Western utilities and regulators should initiate structured knowledge exchange programs with organizations such as the State Grid of China and India’s National Smart Grid Mission (NSGM). Many of the most advanced large-scale grid implementations today are being executed outside the OECD.

Emphasize the Consumer Side of Smart Grid: Demand response, dynamic pricing, and bidirectional metering technologies should be treated as core grid components rather than optional enhancements. Evidence from large-scale deployments shows that consumer-side intelligence can significantly improve grid efficiency and responsiveness.

Embrace Modularity Rather Than Monolithic Mega-Projects: Developing nations are increasingly building grids in modular, interoperable layers that can be upgraded incrementally. In contrast, large monolithic projects in the West often face delays, cost overruns, and single-point vulnerabilities. Modular infrastructure offers greater resilience and adaptability.

Establish Common Standards for Grid Data Architecture at the National Level: Interoperable and open standards for grid and smart metering data are critical for AI-driven optimization. China’s unified AMI framework and India’s emphasis on standardized data systems demonstrate the benefits of coordinated architecture. Fragmented data standards remain a structural disadvantage in Western markets.